China Green Trade Report 2023

JING ZHANG AND CHRISTOPH NEDOPIL | 35-MINUTE READ |

Key findings

- China’s exports of the ‘New Three’—solar photovoltaic (PV), lithium-ion batteries and electric vehicles (EVs)— surged from under USD 20 billion in 2017 to over USD 150 billion in 2023—a growth of 650 per cent.

- Export of the New Three constituted 4.5 per cent of China’s total exports, increasing from 0.86 per cent in 2017.

- China commands 68 per cent, 74 per cent, and 86 per cent of the 2023 global production for electric vehicles, lithium batteries, and solar modules, respectively.

- Major export markets for New Three in 2023 are Europe (USD 66.7 billion, equal to 46.7 per cent of China’s ‘New Three’ exports), North America (USD 17.59 billion—up from USD 2.48 billion in 2017), and East Asia (USD 15.65 billion—11 per cent of China’s ‘New Three’ exports).

- The solar module exports from China in 2023 amounted to around 220 Gigawatts of generation capacity, up 33.5 per cent from 2022’s 164 GW.

- Prices for solar panels per watt have fallen by 30 per cent to USD 0.18 in one year, which has led to a decline in the monetary value of exports of 6.7 per cent from USD 46.3 billion in 2022 to USD 43.7 billion in 2023.

- Asia (in particular Southeast Asia) experienced the largest increase (around 20GW) in 2023 solar module imports from China. Central Asia demonstrated a remarkable growth rate, soaring over 1,000 per cent from USD 45.6 million (8MW) in 2022 to USD 535 million (3.4 GW).

- China’s exports of batteries reached USD 65 billion, reflecting a 27.8 per cent rise compared to USD 51 billion in 2022.

- The US is the main importer of Chinese lithium batteries, though this may change in 2024 due to new policies.

- Exports of (pure) electric vehicles surged to 1,545,832 units, marking a 64 per cent increase from 941,922 units in 2022. This amounted to USD 34 billion, reflecting a 70 per cent rise compared to USD 20 billion in 2022.

- Export of electric vehicles to European countries increased 1500-fold (150,000 per cent) in absolute export values and 174 per cent in vehicle units between 2017 and 2023, from USD 12.55 million to v19.20 billion and from 2,459 to 672,618 vehicles.

- Thailand ascended to the world’s second-largest importer of Chinese-made EVs by volume with 155,910 vehicles, valued at USD 2.5 billion in 2023.

- Russia saw 8,530 electric vehicles imported from China worth USD 263 million, representing a fourfold increase from 2022.

Looking ahead, Chinese policymakers seeing the New Three as a pillar of economic growth will continue to support the industry’s growth.

Western policymakers, meanwhile, worry about dumping, Chinese subsidies, circumvention of trade barriers, human rights, as well as carbon footprint certification posing challenges to Chinese exporters.

Various Chinese manufacturers have reduced export dependencies and invest in local manufacturing including batteries (e.g., EU, US), solar PV (e.g., Vietnam, Malaysia) and NEV parts.

About the data:

This analysis is derived from and presents numbers published by the General Administration of Customs of the People’s Republic of China (GACC)[1].

In trade statistics, the “New Three” include three categories of commodities: solar cells, lithium batteries and electric passenger vehicles.

The HS code of solar cells in 2021 and before is 85414020, and the code in 2022 and after is 854142-854143, including photovoltaic cells that are not installed in modules or assembled into blocks and photovoltaic cells that have been installed in modules or assembled into blocks.

The HS code for lithium-ion batteries is 850760.

The HS codes of electric passenger vehicles are 870220-870240, 870340-870380, including pure electric vehicles and hybrid vehicles, and can be divided into passenger cars with more than 10 seats and small passenger cars with less than 10 seats. The report is based on data related to HS code 870380, which represents over 80 per cent of the overall growth in the EV sector.

Since the earliest accessible data from GACC dates back to 2017, the discussion periods in this report predominantly span from 2017 to 2023.

The currency unit is US dollars unless specified otherwise.

China’s growth of the ‘New Three’

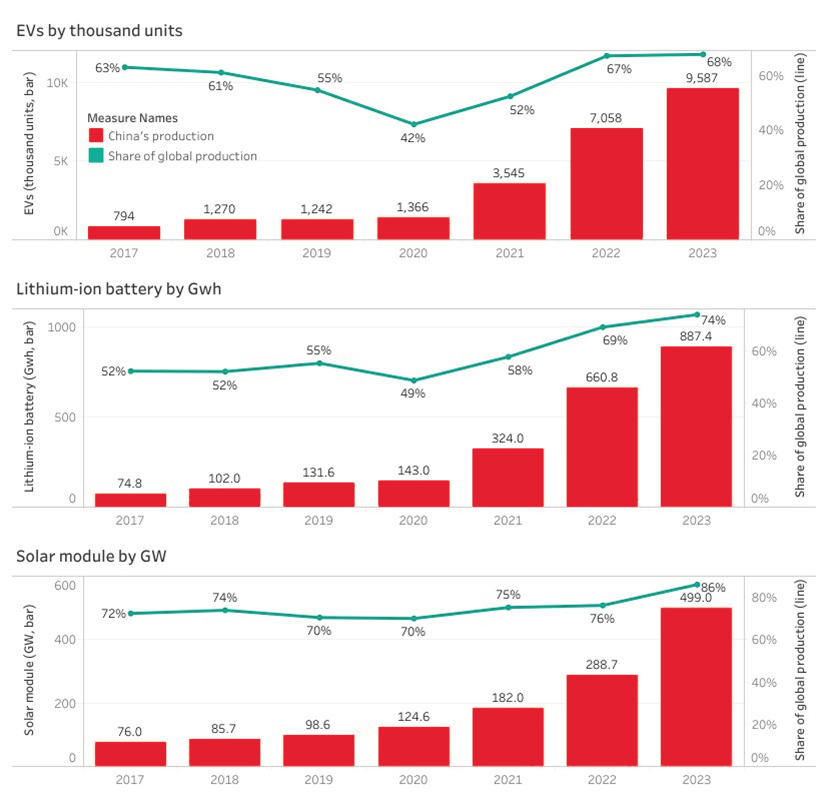

China dominates global trade in batteries, solar PV equipment and to a growing extent electric vehicles—referred to as the ‘New Three’. From 2017 to 2023, China’s solar module production surged from 76 GW to 499 GW, equalling 70 per cent to 86 per cent of global output. In lithium-ion battery production, China’s output rose from 74.8 GWh to 887.4 GWh, with its share ranging from 49 per cent to 74 per cent.

China’s electric vehicle production soared from 794 thousand units to 9,587 thousand units, with its proportion to global output ranging from 42 per cent to 67.6 per cent (Figure 1). The COVID-19 pandemic only led to a temporary production reduction in 2020 coinciding with a significant downturn in production due to weakened consumer demand for electric vehicles.[2]

Figure 1: China’s electric vehicle, lithium battery, and solar module production and their proportion in the global total

China’s exports of ‘New Three’

China’s exports of the ‘New Three’—solar photovoltaic (PV), lithium-ion batteries and electricity vehicles (EVs)—surged from under USD 20 billion in 2017 to over USD 150 billion in 2023—a growth of 650 per cent (Figure 2). During that time, EVs exports soared from USD 312 million to USD 42 billion, equalling an increase of 133 times (13,300 per cent). Lithium battery exports rose from USD 8 billion to over USD 65 billion (plus 713 per cent), and solar panel exports surged from USD 11 billion to USD 44 billion (plus 300 per cent).

Figure 2: China’s export of “New Three” and its share of total exports

From 2022 to 2023, despite a 5.9 per cent decline in China’s overall exports, the “New Three” increased their export value by 21.8 per cent: EVs export values surged by 69.9 per cent, lithium battery export values by 27.8 per cent, while solar panels export values decreased by 5.7 per cent (driven by falling prices per unit, not driven by falling volumes). Accordingly, the New Three’s share of total exports rose from 1.5 per cent in 2020 to 4.5 per cent by the end of 2023. As a comparison, China’s “old three”—clothing, furniture and home appliances, decreased their export share from 12 to 9 per cent during the same period. The largest portion of China’s exports continues to be mechanical and electrical products, accounting for approximately 58.5 per cent of the country’s total export volume in 2023 (Figure 3).

Figure 3: Mechanical and electrical products are fundamental to China’s export strength amidst declines in the Old Three and the rise of the New Three

Regional trends of “New Three” export

Chinese exports of solar panels and lithium batteries reach about 220 countries, while the export destinations of electric vehicles have expanded to 175 countries by 2023, up from 105 in 2017.

Europe has become the major destination of New Three exports, receiving about half (50.74 per cent) of its value in 2022 worth USD 59.5 billion and nearly half (46.7 per cent) in 2023 worth USD 66.7 billion. This is a major change from 2017 when Europe imported goods in these industries worth USD 2.08 billion and constituted only 10.7 per cent of the New Three’s export share (the major export regions used to be South Asia and East Asia). Imports of products from the New Three account for 9.3 per cent of Europe’s total imports (USD 715 billion) from China in 2023.[3]

The export of products related to the New Three to East Asia grew from USD 5.9 billion in 2017 to USD 15.65 billion in 2023. As exports to Europe grew significantly quicker, East Asia’s share of China’s exports of products related to the New Three declined from 30.4 per cent in 2017 to around 11 per cent in 2023.

Similarly, exports to Southeast Asia rose from USD 2.12 billion to USD 11.29 billion, and exports to South Asia from USD 2.09 billion to USD 7.35 billion between 2015 and 2023.

North America’s imports of New Three surged from USD 2.48 billion in 2017 to USD 17.59 billion in 2023 with growth rates of 62.85 per cent in 2021, 95.93 per cent in 2022, and 47.03 per cent in 2023. Between 2021 and 2023, North America’s proportion of China’s total New Three exports increased from 9.4 per cent to 12.3 per cent.

Economies in the Middle East and the Pacific experienced moderate growth of China’s imports from the New Three, while exports to economies in Africa and Central Asia saw significant increases, albeit from relatively lower bases. For instance, Africa’s export value grew from USD 0.53 billion to USD 4.57 billion, and Central Asia’s from USD 8.13 million to USD 2.05 billion. However, their proportions of China’s total export value in New Three remain relatively small (Figure 4andFigure 5).

Figure 4: China’s New Three exports by region

Figure 5: China’s New Three growth across different regions

Sector trends of exports in the “New Three”

Solar PV exports

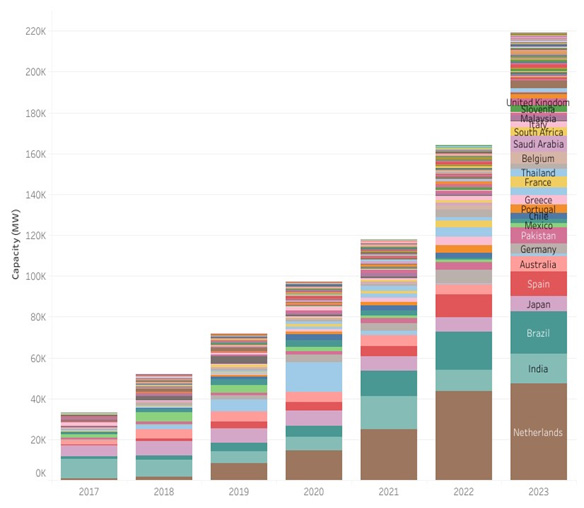

China maintained its dominant grip on the export of solar panels and modules: The total solar module exports from China in 2023 amounted to around 220 Gigawatts (GW) of generation capacity, up 33.5 per cent from 2022 (when about 164 GW capacity was exported), possibly driven by global markets’ efforts to expand clean energy generation.

At the same time, falling prices of solar panels per generation capacity have led to a decline in the monetary value of exports of 6.7 per cent from 2022 (USD 46.3 billion) to 2023 (USD 43.7 billion). Prices per watt declined by 30 per cent, from 25 US cents to approximately 18 cents per watt in just one year (Figure 6). Compared to previous years, the unit price decrease has accelerated: it previously took 5 years for a 10 US cent per watt drop. China’s price reduction stands in contrast to solar production cost for European companies of 24.3 to 30 US cents per watt, and US companies with about 28 US cents.[4]

Figure 6: China’s solar panel exports by region, share & price change since 2017

Europe was the main destination for Chinese solar modules in terms of both export value and capacity, but the region’s share of Chinese solar exports dropped to 48.56 per cent in 2023 from 55 per cent in 2022 by value. The Netherlands was the main port of entry for China’s solar modules for the second consecutive year in 2023, importing 47.2 gigawatts valued at USD 9 billion. Judging from the country’s installation of 4.82 GW of new solar capacity in 2023[5], approximately 90 per cent of these imports can be estimated as being re-exported to other countries or stored for later use.[6] Southern European nations demonstrated solid year-on-year gains in 2023: Turkey’s imports grew by 219 per cent, North Macedonia’s by 192 per cent, Slovenia’s by 141 per cent, and Croatia’s by 100 per cent. Other EU countries, such as Spain, Portugal, and Greece exhibited little growth of direct imports from China, with increases of 10 per cent, 9 per cent, and 6 per cent, respectively. Decreases were observed in Denmark (minus 53 per cent), Hungary (minus 41 per cent), Germany (minus 25 per cent), and Poland (minus 14 per cent) (some of these countries’ panels might have been imported from Netherlands, rather than directly from China).

Asia had the second-largest share of PV exports standing at 21 per cent in terms of export value and 23 per cent in terms of capacity. The region (in particular Southeast Asia) experienced the largest increase (around 20GW) in solar module imports from China in 2023. Nevertheless, the region’s share of China’s exports in solar equipment decreased from its peak of 57 per cent in 2017, with 2022 marking the lowest proportion (18 per cent). India was the largest importing country in Asia in 2023, importing around 14.5 GW of Chinese modules. This surge was likely fuelled not only by demand from utility-scale projects but also by Indian developers stockpiling in anticipation of the April 2024 implementation of the Approved List of Models and Manufacturers (ALMM). The ALMM initiative aims to promote domestic manufacturing capabilities and ease imports in the mid-to-long term. It permits only listed solar PV models and module manufacturers for government-sponsored or subsidized solar projects in India. With the ALMM favouring domestic manufacturers, local production capacity is poised to commence operations in the first half of 2024, potentially reshaping India’s import landscape.[7]

Latin America and the Caribbean had the third-largest share of Chinese solar exports, accounting for 14 per cent in terms of both export value and capacity. Brazil remained the biggest importing country in Latin America and the Caribbean, imported 20.6 GW of Chinese modules, 15 per cent more than 2022’s 17.9 GW. The growing imports of Chinese solar PV to Brazil in recent years were likely supported by its Law 14.300 issued in January 2022 stimulating distributed PV demand and the introduction of a 9.6 per cent import duty in September 2023, accelerating installation efforts. Within Law 14.300, PV projects with a capacity below 5 MW are eligible for net metering until 2045, while small-scale distributed generation projects will incur grid access charges starting in 2023. In addition, the Brazil government removed certain modules from the ex-tariff list (specifying that imported goods qualify for tax exemption only if the functionality exceeds the local manufacturing capacity) in September 2023, imposed a 9.6 per cent import tariff from zero, and introduced a semi-annual tariff rate quota mechanism to safeguard local manufacturing. Stronger demand from utility-scale ground-mounted projects and ongoing construction in late 2023 may lead to growth in module demand for centralized generation projects in Brazil.[8]

The Middle East constituted the fourth-largest share at 6.6 per cent of China’s solar PV exports in terms of export value and 6.4 per cent in terms of export capacity. Large importers in the region, such as the United Arab Emirates experienced a yearly decline in imports (-42 per cent by export capacity and -57 per cent by export value) in 2023, attributed to the completion of significant utility-scale projects, such as mega-projects in Abu Dhabi (Al Dhafra 2 GW) and Dubai (MBR Solar Park Phases 4 and 5, respectively 950 and 900 MW), which resulted in a slowdown in the solar imports. [9] [10]

Africa saw significant increases in module imports from China, surpassing roughly double the combined capacity imported by Pacific and North America, despite starting from a lower base (Figure 7).

Figure 7: Growth/decline of China’s solar panel exports by region

The US directly imported only 539 MW of solar components from China, accounting for 0.3 per cent of total Chinese solar equipment exports In 2023. However, with total imports (including from non-Chinese origins) of solar panels into the US in 2023 being 54 GW[11], re-imports of Chinese equipment from other destinations, partly from Southeast Asian nations, are suspected. Underlying this development preventing US importers from directly importing Chinese solar panels is the US ban on imports of goods made in Xinjiang,[12] a major origin for solar panels, and an additional 25-30 per cent tariffs on solar equipment from China[13]. To reduce re-imports, the US launched an “anti-circumvention” investigation targeting solar products from four Southeast Asian nations—Cambodia, Malaysia, Thailand and Vietnam, aiming to curb Chinese manufacturers from using the region to access the US market. The investigation granted a two-year “exemption period,” expiring in June 2024. Before its expiration, US importers accelerated their purchases, potentially surpassing annual installation capacity (Figure 8).

Figure 8: China’s exports of solar PV to different countries by capacity

Lithium batteries

In 2023, China’s exports of power batteries reached USD 65 billion, reflecting a 27.8 per cent rise compared to 2022 (USD 50.9 billion). This surge is fuelled by China’s robust manufacturing capabilities and its crucial role in meeting the growing global demand for electric vehicles and energy storage solutions.

European economies took the lion’s share (40.06 per cent) of China’s total lithium-ion battery exports (in value) in 2023 (up from 15.17 per cent in 2017). This corresponds to export values increasing from USD 1.2 billion in 2017 to USD 26.04 billion in 2023. Particularly imports to Germany surged from USD 319.27 million in 2017 to USD 9.34 billion in 2023 (an increase of 2,900 per cent) and corresponding to 14.36 per cent of Chinese total lithium batteries exports (up from 4 per cent in 2017). The Netherlands saw import values rise from USD 248.73 million in 2017 to USD 3.64 billion in 2023.

Export values to East Asian economies surged from USD 3.37 billion in 2017 to USD 12.21 billion in 2023, yet its share of China’s total exports of lithium batteries dropped from 42.26 per cent to 18.78 per cent. South Korea’s import value of Chinese-made batteries in 2023 was USD 7.85 billion, a year-on-year increase of 48.8 per cent. Other Asian countries, such as Vietnam, Japan and India, have grown import values of lithium batteries from China over the years, albeit with a slight decrease in their proportions to the total imports. Hong Kong, China, stands out as a distinctive case: Hong Kong has served as a significant transit point for such shipments from the mainland, benefiting from its advanced air cargo and export security inspection systems. However, the heightened regulatory requirements during the pandemic have likely slowed down the processing and transit of lithium batteries through Hong Kong. Possibly driven by this and other factors (e.g., increased costs associated with compliance)[14], may have contributed to a 44 per cent decline in import values of lithium batteries from mainland China (down from USD 2.23 billion in 2017 to USD 1.27 billion in 2023).

Exports to North America grew from USD 1.19 billion in 2017 to USD 14.83 billion in 2023 with North America taking 22.8 per cent of China’s total exports in the sector (up from 15.04 per cent in 2017). The United States was single the largest importer of lithium batteries from China, with import values increasing from USD 1.07 billion in 2017 to USD 13.55 billion in 2023, constituting a 20.84 per cent share of the exports. This may change in 2024, as the US will not extend tax credits to EVs that include internationally sourced components,[15] which also impacts Chinese-sourced batteries.[16] Accordingly, some of the exports to the US might be driven by stockpiling.

Regions like Africa, though from lower bases, showcased remarkable growth in export values. Africa’s battery imports surged from USD 139 million in 2017 to USD 2.36 billion in 2023, marking an increase in its share from 1.74 per cent to 3.62 per cent. South Africa, major markets in Africa, saw a year-on-year increase of 155 per cent in 2023.

South Asia’s exports rose from USD 72.31 million in 2017 to USD 238.50 million in 2023. Meanwhile, Middle Eastern economies saw moderate increases, reaching USD 734 million in 2023 from USD 72.31 million in 2017. However, Central Asia’s imports only slightly grew, reaching USD 36.12 million in 2023 from USD 34.85 million in 2017 (Figure 9 and Figure 10).

Figure 9: China’s lithium battery exports by regions since 2017

Figure 10: China’s exports of lithium batteries to different countries by value

Electric vehicles[17]

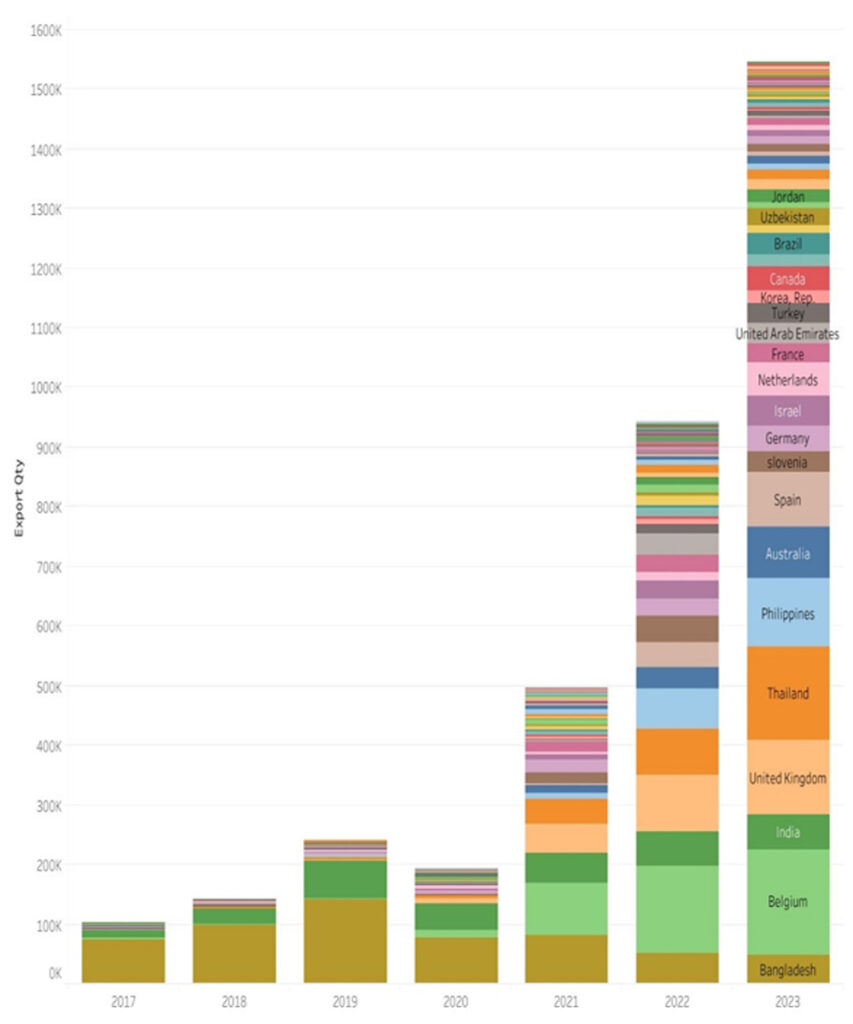

In 2023, China saw a surge in electric vehicle exports, reaching 1,545,832 units, marking a 64 per cent increase from 2022 (941,922 units). This amounted to USD 34 billion, reflecting a 70 per cent rise compared to 2022 (USD 20 billion).

The export of electric vehicles to European countries witnessed a 1500-fold (150,000 per cent) increase in absolute export values, from USD 12.55 million in 2017 to USD 19.20 billion in 2023. Within Europe, EU economies received about USD 7.4 billion in EV imports from China in 2023—with the rest going to non-EU European countries. Europe’s share peaked at 80.89 per cent in 2020 before falling to 56.28 per cent by 2023, highlighting the dynamic nature of the European market. In 2023, Belgium was the top entry port that received 175,437 electric vehicles from China. Russia witnessed a significant upward trend in electric vehicle imports from China as well, with import value increasing from USD 53 million in 2022 to USD 263 million in 2023 (a fourfold increase) and import quantity rising from 3110 units to 8,503 units (rising 173 per cent).

Southeast Asia is the second largest market for Chinese EV exports, receiving USD 3.16 billion in 2023 (up from USD 6.9 million in 2017). Thailand ascended to the world’s second-largest importer of Chinese-made EVs by volume with 155,910 vehicles, marking a 104 per cent increase compared to 2022, and the fourth-largest by value (USD 2.5 billion), representing a 442 per cent increase from 2022. One reason might be Thailand’s ambition to achieve 30 per cent zero-emission vehicles in its total automotive production by 2030 through its electric vehicle development roadmap. The EV3.0 scheme, initiated in June 2022, offers cash subsidies for imported passenger electric vehicles, providing an opportunity for Chinese EV firms like SAIC Motor, BYD, Great Wall Motors, and Neta Motors, all of which have established factories in Thailand.[18]

| Rapid innovation in the Chinese New Energy Vehicle Space Within the past decade, Chinese companies have become world-leading developers in new energy vehicles (NEVs) due to a combination of rapid innovation, daring innovation in business models and government support for the production and domestic sales of NEVs. As an example: in 2023, BYD overtook Tesla to become the largest NEV car manufacturer by volume. BYD was founded in 1995 in Shenzhen supplying batteries for mobile phones. It expanded its business model to build cars and has now become a world-leading manufacturer of a wide array of electric cars, buses, trucks, and energy storage systems. The company has established or is in the process of building nine vehicle factories in key cities nationwide, including Shenzhen, Xi’an, Changsha, Changzhou, and Hefei, aiming for a combined annual production capacity of 5.82 million vehicles. Furthermore, in response to policy uncertainties affecting Chinese EV exports to key markets like the US and Europe, BYD has strategically expanded its production footprint to more favourable regions such as Thailand, Brazil, Indonesia, Hungary, and Uzbekistan, with Mexico also on the radar for future expansion. Similarly, Xiaomi, a company founded in 2010 in Beijing, established itself as a producer of electronics for everyday use at affordable prices. In 2024, it introduced its first electric vehicle SU7 with much fanfare and pre-orders worth 88,898 in the first 24 hours (as a comparison, Volkswagen’s ID.7 model to be introduced in December 2023 only received a mere 300 preorders in its first 72 hours.[19] As a consequence of China’s rapid growth and leadership in the space, traditional car manufacturers, such as Ford, Volkswagen or BMW are seeking new partnerships with Chinese producers and expanding their investments in China also to significantly accelerate product development. |

Similarly, from 2017 to 2023, the Philippines experienced a significant increase in electric vehicle imports from China, rising from 961 units to 115,423 units (120 times). Despite this, as the per unit price remained relatively low compared to other countries, trade value increased “only” from USD 0.57 million to USD 97.15 million (170 times). The surge in imports can be attributed to the Philippines’ decision to temporarily waive the 30 per cent tariffs on imported electric vehicles, spanning cars, minibuses, vans, buses, trucks, tricycles, motorcycles, and bicycles, for a period of five years since 2023.[20]

The Pacific region saw a remarkable increase in its share of China’s electric vehicle exports, rising USD 0.48 million to USD 2.70 billion and taking 7.92 per cent of Chinese EV exports in 2023. Australia (counted as a Pacific country for the purpose of this study) imported 86,437 EV units worth USD 2.35 billion. This aligns with the goals set by major Australian states, including Sydney, Melbourne, and Brisbane, to achieve 50 per cent of all new car sales to be electric by 2030. These states offer generous rebates (maximum AUD 6,000) and are investing in charging infrastructure, driving the demand for electric vehicles in Australia.[21]

Central and East Asia each imported approximately USD 1.5 billion worth of electric vehicles from China. Central Asia’s imports rose from USD 0.85 million in 2017 to USD 1.5 billion in 2023, reflecting a significant expansion in market presence. Uzbekistan, the Kyrgyz Republic, and Kazakhstan imported USD 623 million, USD 429 million, and USD 329 million, respectively, totalling at USD 1.38 billion in 2023. East Asia increased Chinese EV imports from USD 9.55 million in 2017 to USD 1.5 billion in 2023 (equivalent to a share of China’s total EV exports fluctuated, starting at 8.68 per cent in 2017, declining to 1.18 per cent in 2020, before rebounding slightly to 4.42 per cent in 2023). Notably, Hong Kong, Korea, and Japan experienced year-on-year increases of 23 per cent, 167 per cent, and 36 per cent, respectively, in 2023.

Export values to South Asia increased from USD 72.31 million in 2017 to USD 238.50 million in 2023 (a 230 per cent increase). With much faster growing exports to other markets, the region’s share of Chinese EV exports dropped from 65.76 per cent in 2017 to 0.70 per cent in 2023. The Indian and Nepalese markets have experienced moderate growth, while the import value of Bangladesh has declined by about one-third compared to 2017.

Chinese-made electric vehicles haven’t played a sizable role in the US market. China directly shipped just 12,363 EVs to the US worth USD 332 million in 2023. This is largely due to the 27.5 per cent import tariffs on Chinese-made cars and other regulatory barriers. In contrast, exports to Canada reached USD 1.6 billion, raising concerns about EV trade “leakage” from Canada to the US.

Finally, the Middle Eastern economies showed significant increases in their proportions, rising from 1.6 million in 2017 to 2.4 billion in 2023, signalling a burgeoning market presence. Israel’s imports surged to 50,541 units valued at USD 1.3 billion in 2023, reflecting a year-on-year increase of 47 per cent by value and 67 per cent by units (Figure 11and Figure 12).

Figure 11: EVs exports focus on Europe and Southeast Asia

Note: The above chart does not include China’s exports of plug-in hybrid electric vehicles, which use batteries to power an electric engine and fuel to power an internal combustion engine.

Figure 12: China’s exports of electric vehicles to different countries by quantity

Outlook for China’s New Three export

Understanding China’s New Three manufacturing and trade is crucial to address global green transition goals. Yet navigating the sector for both investors and producers remains challenging. Particularly Western policymakers are concerned about Chinese dominance in the sector and about overcapacity in China which would lead to potential dumping prices and threaten domestic manufacturers outside China. Thus, both the US Treasurer Yellen and German chancellor Scholz in their recent visits to China highlighted the need to address overcapacity. Discussions on ramping up trade barriers including measures of anti-dumping, anti-subsidy, anti-circumvention, increased tariffs, and emerging obstacles such as “human rights”, “carbon footprint certification”, and “energy efficiency labels” could pose obstacles for further development of the sector.

Meanwhile, Chinese policy makers view the New Three industry as an important pillar for structural reform of China’s economy. In December 2023 China’s, Ministry of Commerce and eight other ministries including the Foreign Ministry and the central bank released Opinions on supporting the healthy development of new energy vehicle trade cooperation, pledging to support the globalization efforts of Chinese EV makers in the NEV trade cooperation. China’s President Xi highlighted the benefits of cheap exports to Europe to German Chancellor Scholz in April 2024. At the same time, Chinese policy makers also note overcapacity in the sector, as evidenced at Premier’s Qiang’s Government Work Report delivered at the Two Sessions in February 2024.

At this time, however, Chinese dominance in these three sectors is unlikely to be challenged due to a very well-integrated value chain, rapid innovation, industrial synergies, economies of scale, and continuous governmental support that allow Chinese producers to be both affordable and technology leaders. Paired with a continuous demand for affordable new energy solutions from both developed and even more so from emerging economies (e.g., in the Belt and Road Initiative) demand for solar PVs, battery storage and new energy vehicles is expected to rise and Chinese producers are posed to maintain their advantage in the New Three industries.

With technological development (e.g., rapidly declining cost for solar panels and batteries), volumes and value of exports might develop differently (i.e., growing volumes, stagnating values). Also regionally, we expect new developments due to uncertainty in trade policies particularly from developed economies.

An example is the US Inflation Reduction Act, which presents challenges for Chinese made lithium batteries (and similarly lithium batteries produced by Chinese-owned manufacturers). Moreover, Chinese electric vehicle exports to Europe encounter increasing resistance due to economic and security concerns, compounded by the European Commission’s investigation into potential subsidies in China’s BEV value chains violating EU or WTO rules.

Circumventing some of the growing concerns on international trade, producers of Chinese New Three product are pursuing overseas investments. For example, Chinese producers plan about 400GWh of battery production capacity in Europe, representing nearly one thirds of Europe’s total capacity. While plans for battery factory construction in the United States are more conservative due to geopolitical factors and tariffs, examples of Chinese investments exist, such as Gotion High-tech, which announced a $4.36 billion plan for battery plants in Illinois and Michigan or EVE Energy $150 million investment in a joint venture with Daimler Truck, Electrified Power and Paccar, in a 21 gigawatt-hours US battery plant. Chinese battery companies are also pushing their upstream suppliers to offer nearby support for overseas capacity expansion, prompting upstream lithium battery firms like Tianci Materials and Senior Technology to establish subsidiaries in Europe, with Easpring Material, CNGR Advanced Material, and Finnish Minerals Group also expanding their production capacity.

To secure longer term growth and technological development, China should cooperate with foreign investors and partners to develop more joint ventures and allow for Western companies to enter the market more freely, all while addressing concerns of unfair subsidies for Chinese manufacturers. Over the past years, policymakers have already promised to further open various sectors to foreign investment while reducing local advantages and improving financing access. For instance, China’s recent announcement completely remove market access restrictions on foreign investment in manufacturing, including high-end manufacturing. Financial institutions are encouraged to provide high-quality financial services and support to qualified foreign-invested projects.

About the authors

Dr Jing ZHANG is a Research Fellow working jointly at the Griffith Asia Institute and the University of Queensland. She is an economist with a diverse range of expertise encompassing agricultural systems, natural resource management, government policy and the international trade. She has developed advanced skills in statistical, market and policy analysis, coupled with extensive experience and valuable connections within the Asia-Pacific. In her current role at Griffith Asia Institute, she is focused on acquiring expertise in green finance.

Dr Christoph NEDOPIL is the Director of the Griffith Asia Institute and a Professor at Griffith University in Brisbane, Australia. He is also a Visiting Professor at FISF Fudan University, Shanghai, Acting Director of the Green Finance & Development Center at FISF Fudan University, and a Visiting Faculty at Singapore Management University (SMU).

Christoph regularly provides advisory to governments, financial institutions, enterprises, and civil society on sustainable development issues. He is the lead author of the UNDP SDG Finance Taxonomy, the Innovative Climate Finance Solutions report for the G20 in Indonesia, and the Green Development Guidance of the BRI Green Development Coalition under the Chinese Ministry of Ecology and Environment. He has authored four books and published articles in Science and other leading journals. Christoph serves as board director in scaling sustainability in businesses and finance.

Christoph is quoted regularly in Financial Times, The Economist, Reuters, Bloomberg, and other major outlets. Before joining Griffith University, he served as Founding Director of the Green Finance & Development Center and Associate Professor at the Fanhai International School of Finance (FISF), Fudan University and previously as Founding Director for the Green BRI Center at the Central University of Economics in Beijing. He worked with the World Bank in over 15 countries and was a Director in the German development agency GIZ. Christoph holds a Master of Engineering and a PhD in Economics from the Technical University Berlin, as well as a Master of Public Administration from Harvard Kennedy School.

[1] http://stats.customs.gov.cn/

[2] W. Wen et al., ‘Impacts of COVID-19 on the Electric Vehicle Industry: Evidence from China’, Renewable and Sustainable Energy Reviews 144 (1 July 2021): 5, https://doi.org/10.1016/j.rser.2021.111024.

[3] China shipped USD 3.389 trillion worth of exported products around the globe in 2023. Nearly half (47.8 per cent) was delivered to fellow Asian countries while another 21.1 per cent was sold to importers in Europe. China shipped 18.6 per cent worth of goods to buyers in North America. Smaller per centages went to customers in Africa (5.1 per cent), Latin America (4.8 per cent) excluding Mexico but including the Caribbean, Africa (4.6 per cent), and Oceania (2.6 per cent) led by Australia and New Zealand. https://www.worldstopexports.com/chinas-top-10-exports/?expand_article=1

[4] Keith Bradsher, ‘How China Came to Dominate the World in Solar Energy’, The New York Times, 7 March 2024, sec. Business, 3, https://www.nytimes.com/2024/03/07/business/china-solar-energy-exports.html.

[5] Anu Bhambhani, ‘Netherlands Installed 4.82 GW New Solar Capacity In 2023’, TaiyangNews (blog), 26 March 2024, 10, https://taiyangnews.info/netherlands-installed-4-82-gw-new-solar-capacity-in-2023/.

[6] Statistics Netherlands, ‘The Netherlands Largest Importer of Chinese Solar Panels’, webpagina, Statistics Netherlands, 8 September 2023, 10, https://www.cbs.nl/en-gb/news/2023/36/the-netherlands-largest-importer-of-chinese-solar-panels.

[7] India Briefing, ‘India Reinstates ALMM for Solar PV Modules’, India Briefing News, 8 April 2024, 13, https://www.india-briefing.com/news/india-approved-list-models-manufacturers-almm-solar-pv-modules-31894.html/.

[8] ‘Module Imports to Decrease in Early 2024 after Persisting Last Month-Industry-InfoLink Consulting’, 13, accessed 15 April 2024, https://www.infolink-group.com/energy-article/solar-topic-module-imports-decrease-in-early-2024-after-persisting-last-month.

[9] Gavin Maguire and Gavin Maguire, ‘China Steers Solar Module Export Stream towards Asia’, Reuters, 28 February 2024, sec. Commodities, https://www.reuters.com/markets/commodities/china-steers-solar-module-export-stream-towards-asia-2024-02-28/.

[10] ‘United Arab Emirates’ solar market’, pv magazine International, 5 May 2023, 13, https://www.pv-magazine.com/2023/05/05/united-arab-emirates-solar-market/.

[11] ‘“Extreme Dependence”: US Solar Panel Imports Boom to Record 54 GW in 2023’, 11, accessed 5 April 2024, https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/extreme-dependence-us-solar-panel-imports-boom-to-record-54-gw-in-2023-80448513.

[12] ‘Crackdown on China’s solar industry casts long shadow’, Australian Financial Review, 17 March 2024, 14, https://www.afr.com/world/asia/crackdown-on-china-s-solar-industry-casts-long-shadow-20240315-p5fcq3.

[13] ‘U.S. Political Landscape and Solar Policy Trajectory -Industry-InfoLink Consulting’, 14, accessed 15 April 2024, https://www.infolink-group.com/energy-article/solar-topic-political-landscape-solar-policy-trajectory-in-the-US.

[14] Dimerco, ‘Advantages of Hong Kong as a Trans-shipment Hub for South China Manufacturers’, Dimerco, 15 December 2023, 16, https://dimerco.com/advantages-of-hong-kong-as-a-trans-shipment-hub-for-south-china-manufacturers/.

[15] David Shepardson, ‘More EVs Lose US Tax Credits Including Tesla, Nissan, GM Vehicles’, Reuters, 2 January 2024, sec. Autos & Transportation, 13, https://www.reuters.com/business/autos-transportation/more-evs-lose-us-tax-credits-including-tesla-cybertruck-nissan-leaf-2024-01-01/.

[16] Currently, tax benefits exclude batteries sourced from companies incorporated or headquartered in China, as well as firms with 25 per cent of board seats or equity interest held by Chinese governments. Chinese owned companies with headquarters outside of China might be exempt and Chinese battery manufacturers accordingly venture into developed markets.

[17] The analysis primarily centres on pure EVs (HS code 870380: motor vehicles for transporting fewer than 10 persons, with only electric motor propulsion) due to their substantial contribution, over 80 per cent, to the overall growth in the EV sector. However, it’s noteworthy to mention the significant development of other electric vehicles that fall under the following HS codes:

870220 – Motor vehicles for transporting 10 or more persons, with both diesel engine and electric motor propulsion

870230 – Motor vehicles for transporting 10 or more persons, with spark-ignition engine and electric motor propulsion

870240 – Motor vehicles for transporting 10 or more persons, with only electric motor propulsion

870340 – Motor vehicles for transporting fewer than 10 persons, with spark-ignition engine and electric motor propulsion

870350 – Motor vehicles for transporting fewer than 10 persons, with diesel engine and electric motor propulsion

870360 – Motor vehicles for transporting fewer than 10 persons, with spark-ignition engine and electric motor propulsion, capable of external electric power charging

870370 – Motor vehicles for transporting fewer than 10 persons, with diesel engine and electric motor propulsion, capable of external electric power charging

[18] ‘China EV drive into Thailand galvanised by smog and subsidies, ASEAN Business – THE BUSINESS TIMES’, 5 February 2024, 12, https://www.businesstimes.com.sg/international/asean/china-ev-drive-thailand-galvanised-smog-and-subsidies.

[19] Peter Johnson, ‘Volkswagen’s Flagship ID.7 EV Is off to a Slow Start in China, with Only 300 Orders in 3 Days’, Electrek, 19 December 2023, 19, https://electrek.co/2023/12/19/volkswagen-id-7-fails-impress-china-300-orders/.

[20] ‘Philippines: The Electric Vehicle Industry Development Act (EVIDA), Republic Act No. 11697, Lapses into Law’, 19, accessed 16 April 2024, https://insightplus.bakermckenzie.com/bm/tax/philippines-the-electric-vehicle-industry-development-act-evida-republic-act-no-11697-lapses-into-law.

[21] Stella Qiu, ‘BYD Spearheads Chinese Electric Car Push in Australia, a Friendlier Market’, Reuters, 8 March 2024, sec. Autos & Transportation, 18, https://www.reuters.com/business/autos-transportation/byd-spearheads-chinese-electric-car-push-australia-friendlier-market-2024-03-05/.