China green finance status and trends 2025-2026

FANG YANG, JINZE LI AND CHRISTOPH NEDOPIL

1. Introduction

China’s green finance development in 2025 continued to make significant progress across several areas. This advancement contrasts with trends in many Western markets, which have slowed or, in the case of the United States, reversed progress on green and sustainable finance. China’s advancements in green finance appear to be driven by three factors:

- Policy trumps politics: unlike many Western countries, Chinese politics is less public, allowing policymakers to focus more on policy development. This enables the evaluation of environmental risks, such as climate change and biodiversity loss, based on scientific evidence rather than populism or current voter sentiment. As a result, policy recognises the need for green finance to address both short-term and long-term financial risks associated with climate change. This also reflects another feature of China’s system – long-term planning, in contrast to the shorter political election cycles in many Western countries.

- Green economy opportunities: China is increasingly capitalising on the economic opportunities presented by a green transition, supported by a growing green real economy (e.g., in renewable energy, electric vehicles, and green industrialisation). These opportunities manifest in green economy equipment (e.g., solar PV panels, wind turbines, batteries) as well as in the cost advantages of a green transition (e.g., lower energy prices)

- Green finance knowledge and capacity in key institutions: Key institutions, such as the People’s Bank of China (PBoC) (China’s central bank) and related government and non-government entities (both financial and non-financial), have developed strong expertise in green finance since the top-level establishment of China’s green financial system in 2015. Although significant gaps persist across the financial ecosystem, China’s green finance capacity is likely world-leading, enabling it to export its knowledge base (e.g., through the Green Investment Principles (GIP), the Global Green Finance Leadership Program (GFLP), and the Capacity Building Alliance of Sustainable Investment (CASI).

In 2025, China’s green finance development continued to receive support from top party organs as well as through China’s government ministries and regulators (e.g., in the recommendations for the 15th Five-Year Plan 2026-2030). Specific progress was made in enhancing the standardisation of green finance through a new unified green taxonomy (previously, China had several green finance taxonomies, e.g., credit and bonds) and a statistical system. China also strengthened green insurance, impacting both the insured assets and the invested assets of insurance companies. Key developments included the expansion of the emission trading system to encompass steel and other sectors, along with a commitment to shift from intensity-based to absolute emission caps within the next five-year plan. Transition finance continues to play a vital role, though progress in standardisation has been gradual.

The application of green finance, measured by metrics such as green bonds issuance or green credit utilisation, remained generally stable over the past year, with growth in green credit, a recovery in green bonds from a low in 2024, and a stable outlook for green funds. As in previous years, it is worth noting that labelled green finance represents only a fraction of China’s overall financial system, with green bonds accounting for about 1% of all issued bonds and green loans comprising about 16% of all loans.

Building on the previous reports for 2022-23,[1] 2023-24[2] and 2024-25,[3] this brief analyses China’s green finance policies in 2025, identifies key trends, and recommends actions to further scale green finance. It serves as a snapshot of key developments and uses specific examples to illustrate China’s green finance trends and directions. It is not intended as a comprehensive guide to Chinese green finance and its developments.

2. Progress on China’s green finance policies in 2025

China’s overall policies supporting green transition and development strengthened in 2025. Both the Fourth Plenum (October 2025)[4] and the CPC Central Committee’s Proposal on the 15th Five-Year Plan (issued in October 2025) emphasise the carbon reduction goals and green industrial development, including the goal to “vigorously develop science and technology finance, green finance, inclusive finance, pension finance, and digital finance”.[5]

The following sections highlight and analyse green finance policy developments in China based on the five pillars for green finance development outlined by the PBoC since 2021:[6]

- Improve the green finance standard system;

- Strengthen regulation and disclosure requirements;

- Enhance the incentive and restraint mechanisms;

- Enrich the product and market system; and

- Expand international cooperation and lead the setting of international standards for green finance.

2.1 Standard system

Progress has been made in standard systems for green classification, statistical systems, green finance terminology, green insurance, transition finance, and biodiversity finance.

2.1.1 Green taxonomy

The People’s Bank of China (PBoC), the China Banking and Insurance Regulatory Commission (CBIRC), and the China Securities Regulatory Commission (CSRC) jointly issued the Green Finance Support Project Catalogue (2025 Version), effective October 1, 2025. This represents a crucial step in transitioning China’s green finance standards system from multiple parallel tracks toward unification.[7] The 2025 Catalogue was revised based on the Guidance Catalogue for Green and Low-Carbon Transition Industries (2024 Version) and the Green Bond Support Project Catalogue (2021 Version). It unifies the original green bond support standards, the green loan statistical criteria of the People’s Bank of China, and the green loan statistical criteria of the Financial Regulatory Administration (formerly the China Banking and Insurance Regulatory Commission).

Compared to the Green Bond Support Project Catalogue (2021 Version), the scope of supported green sectors has expanded significantly in the 2025 Version: The 2025 Version builds on the seven green industry categories outlined in the Guidance Catalogue for Green and Low-Carbon Transition Industries (2024 Version)—energy conservation and carbon reduction, environmental protection, resource recycling, green and low-carbon energy transition, ecological conservation, restoration, and utilization, green infrastructure upgrades, and green services—and adds two new categories: green trade and green consumption. These categories are further subdivided into 38 secondary categories and 271 tertiary categories. As such, the categorisation aligns with the three-tier classification system of China’s national economic industry codes.

Hong Kong’s Monetary Authority (HKMA) launched a public consultation on the prototype for Phase 2A of the Hong Kong Sustainable Finance Taxonomy, with plans to eventually incorporate it into banking regulatory policies.[8] The updated taxonomy adds manufacturing and information and communications technology sectors, expanding coverage from 4 to 6 industries and increasing economic activities from 12 to 25. It introduces definitions for “transition” and “climate adaptation” categories for the first time, specifying that transition activities should achieve significant emissions reductions in the short term. The initial phase of the framework has been piloted by select banks and enterprises, covering key sectors such as power generation and construction. While the updated framework remains voluntary, it could eventually influence approximately HKD 8.6 trillion (USD 1.1 trillion) in banking sector asset allocation.

2.1.2 Statistical system

In April 2025, the PBoC, National Financial Regulatory Administration (NFRA), CSRC, and the State Administration of Foreign Exchange (SAFE) jointly issued the Comprehensive Statistical System for the “Five Major Tasks” (Trial Version).[9] This system establishes unified provisions for statistical subjects and scope, statistical indicators and definitions, statistical recognition standards, data collection, sharing, and release, as well as departmental responsibilities related to the “Five Major Tasks”.

The system clarifies that statistical subjects encompass financial institutions such as banks, securities firms, and insurance companies, as well as financial infrastructure institutions. The statistical scope covers various financial instruments and products, including loans, bonds, equities, asset management, debt, funds, and insurance. Additionally, it establishes over 200 key statistical indicators covering financing, digital transformation of financial institutions, and other areas, effectively aligning with national statistical standards, industry policies, and the comprehensive financial statistics system.

2.1.3 Green finance terminology

In March 2025, the State Administration for Market Regulation (SAMR)[10] and the Standardisation Administration of China (SAC) released the national standard Green Finance Terminology (GB/T 45490-2025).[11] Drafted under the leadership of the People’s Bank of China, this standard defines general terms and specialised terminology in related fields of green finance. It covers classifications such as green credit, green securities, green insurance, environmental equity, carbon markets and carbon finance. Applicable to finance, management, research, and education sectors, this marks China’s first national standard in the green finance domain. The standard eliminates previous discrepancies across multiple metrics in green credit and introduces specialised terminology such as energy efficiency credit, aligning with the updated green industry catalogue. In the green securities sector, previously fragmented definitions of green bonds have been consolidated. Terms such as sustainability bond, green asset-backed security, and green guarantee are included for the first time, establishing terminological alignment with ESG investing. Green insurance coverage expands beyond pollution liability insurance to encompass all categories of green risk protection. Environmental equity is defined for the first time at the national standard level, covering eight categories, including pollution discharge permit, energy-using permit, and renewable energy certificate, along with environmental equity finance. The carbon markets and carbon finance establish a comprehensive terminology chain from carbon emission permit, carbon allowance, and China Certified Emission Reduction (CCER) to carbon options, carbon lending, and carbon fund, resolving previous conceptual overlaps and providing a unified terminology benchmark for green finance operations across all sectors.

2.1.4 Green insurance

Focusing on advancing the “Five Major Tasks”,[12] in accordance with the Guiding Opinions on Advancing the “Five Major Tasks” in the Banking and Insurance Sectors, the NFRA and the PBoC jointly issued the Implementation Plan for High-Quality Green Finance Development in the Banking and Insurance Sectors in February 2025.[13] This plan emphasises that insurance companies should develop targeted risk protection solutions to serve the green transition, enhance the quality and efficiency of green insurance operations, and strengthen the utilisation of insurance funds. This includes participating in green project investments through green bonds, green asset-backed securities, and insurance asset management products. On the asset side, insurance funds are guided to increase allocations to green bonds, green projects and green equity funds. ESG and climate-related factors are progressively integrated into underwriting, pricing and investment decision-making, supported by strengthened green insurance risk assessment models.

2.1.5 Transition finance

The PBoC has made significant progress in leading the development of financial standards for the transformation of four key industries: steel, coal-fired power, building materials, and agriculture. Wang Xin, Director of the Research Bureau of the PBoC stated:

“We have also developed implementation guidelines to clarify the criteria for identifying transition entities, effectively addressing the reasonable and necessary funding needs of traditional high-carbon sectors during their low-carbon transformation”.

These standards are currently being piloted in select regions, including Fujian, Sichuan, and Shanxi, where they have been well-received by the market. Wang further revealed that the development of transition finance standards for a second batch of seven sectors, including shipping and chemicals, is underway.

Additionally, local governments and financial institutions are actively exploring transition finance standards for 2025:

- Jiangsu: In February, the Notice on Establishing a Transition Finance Support System to Facilitate Jiangsu’s Comprehensive Green and Low-Carbon Transition was issued.[14] This document outlines the overall objectives for Jiangsu’s transition finance efforts. It proposes establishing a “1+N+N” transition finance support system, comprising 1 set of evaluation criteria for transition finance entities, N catalogues of transition finance-supported economic activities, and N types of transition finance products and service models, guided by the principle of “benchmarking internationally, grounded in reality, and demand-driven”. This system aims to align with Jiangsu’s industrial structure, energy mix, and high-quality development needs to channel financial resources toward supporting the green and low-carbon transformation of traditional industries. The notice also released the first catalogue of economic activities supported by Jiangsu’s transition finance. Covering eight major industries—petrochemicals, chemicals, steel, nonferrous metals, printing and dyeing, shipping, building materials, and papermaking—the catalogue provides concrete guidance for enterprises to formulate scientifically feasible transition plans.

- Guangzhou: The Guangzhou Transition Finance Implementation Guide group standard was formally released and implemented in December.[15] This standard establishes a transition finance support project catalogue for three industries: chemical raw materials and chemical products manufacturing, pharmaceutical manufacturing, and rubber and plastic products manufacturing. As Guangzhou’s first transition finance standard, it provides comprehensive guidance for conducting transition finance operations.

- Hebei: Based on the revised Hebei Province Steel Industry Transition Finance Work Guidelines (2023-2024 Version), the Hebei Province Steel Industry Transition Finance Work Guidelines (2025 Version) were developed.[16] This updated version further focuses on challenging issues within steel enterprises, establishing a comprehensive policy support system.

2.1.6 Biodiversity finance

To enhance the targeted and effective financial support for biodiversity conservation, the PBoC has spearheaded the development of the Biodiversity Finance Catalogue (Trial Version) in 2025. Currently undergoing pilot implementation in select regions, including Hubei, Fujian, and Tianjin, the initiative aims to advance formal adoption and implementation once sufficient experience is gained. The catalogue encompasses four major categories totalling 87 entries: sustainable utilisation of biological resources, ecosystem conservation and restoration, nature-based solutions (NbS), and environmentally friendly activities in highly sensitive industries. Compared to previous catalogues, it introduces 24 new entries.[17]

2.1.7 China-EU Common Ground Taxonomy (CGT)

Building upon the Phase I outcomes of the 2021 China-EU Common Ground Taxonomy (CGT), the expanded China-EU Common Ground Taxonomy (2024 Version) and its multilateral derivative, the Multi-jurisdiction Common Ground Taxonomy (M-CGT) were released in 2024. With the publication of the M-CGT, the Monetary Authority of Singapore (MAS) has spearheaded efforts to expand bilateral EU-China CGT to include the Singapore-Asia Taxonomy (SAT),[18] enhancing the interoperability of taxonomies across China, the EU and Singapore.

CGT and M-CGT aligned bonds are labelled by an expert panel of the Green Finance Committee of the China Society for Finance and Banking (CSFB) through monthly CGT labelling.

Furthermore, the National Association of Financial Market Institutional Investors (NAFMII) has expanded its use of the China-EU Common Ground Taxonomy: Climate Change Mitigation and the EU Taxonomy Climate Delegated Acts as criteria for green project certification, in accordance with the China Green Bond Principles.[19] This has further optimised the mechanism for overseas institutions issuing green panda bonds, effectively enhancing convenience.

Additionally, Australia has actively engaged in this international coordination process. In June 2025, the inaugural roundtable of the Australia-China Sustainable Finance Taxonomy Roadmap project took place in Canberra. Participants recognised that, despite differences between the two countries’ taxonomies, identifying common ground through processes such as the M-CGT is key to enhancing sustainable capital flows between Australia and China. Further dialogues were held in Beijing and Hong Kong later in 2025.[20]

Table 1: Key trends in China’s green finance standard system

| Positive progress | Challenges |

| Standardise statistical definitions for green loans and green bonds, and refine statistical systems and indicator frameworks;Issue the first national standard for green finance terminology;Pilot and promote financial standards for transition in four key industries, with local supporting policies implemented concurrently. | National transition finance standards for key industries have not yet been finalised;The same catalogue for “green” and “low-carbon transition” sectors may confuse identification;Blue finance standards are still under development, and small and medium-sized institutions lack the capacity to adapt to these standards. |

Environment minister Huang Runqiu speaks at the COP30 China pavilion (Image: Kiara Worth / UN Climate Change, CC BY-NC-SA)

2.2 Disclosure policy

China made further progress in disclosure policies for companies, especially financial institutions and listed companies.

In September 2025, in accordance with the Corporate Sustainable Disclosure Guidelines—Basic Guidelines (Trial Version) issued in 2024, the Ministry of Finance (MoF), in collaboration with the Ministry of Foreign Affairs (MoFA), the National Development and Reform Commission (NDRC), the Ministry of Industry and Information Technology (MIIT), the Ministry of Ecology and Environment (MEE), the Ministry of Commerce (MOFCOM), the PBoC, SASAC, NFRA, and CSRC, formulated and issued the Application Guidelines for the Corporate Sustainability Disclosure Standards—Basic Standards (Trial Version).[21] This guide consists of nine questions covering the value chain, reporting entity, information relevance, primary users of sustainability information, materiality assessment, the principle of proportionality, current and projected financial impacts of sustainability risks and opportunities, resilience of the enterprise’s strategy and business model to sustainability risks, and sustainability impact disclosure. Considering the developmental stage and disclosure capabilities of Chinese enterprises, the implementation of corporate sustainability disclosure standards will not adopt a one-size-fits-all mandatory approach. Instead, it will follow a strategy of prioritising key areas, piloting initiatives first, advancing progressively, and implementing in phases. This approach will expand from listed companies to non-listed companies, from large enterprises to small and medium-sized enterprises, from qualitative requirements to quantitative requirements, and from voluntary disclosure to mandatory disclosure. The Guidelines are based on the International Sustainability Standards Board (ISSB) Standards, “aligning with China’s context and showcasing Chinese characteristics”.[22]

In October, China Central Depository & Clearing Co., Ltd. released six corporate standards, including the China Bond Green Finance Environmental Benefit Disclosure Indicator System, to complement the Green Finance Support Project Catalogue (2025 Version) issued by PBoC and other departments.[23] The new standards aim to improve compatibility and consistency in environmental benefit disclosure for green financial products such as green bonds and green loans, further refining the green finance standards system. It specifies the essential elements, coding specifications, and indicator system for environmental benefit disclosure in green finance. It proposes quantitative environmental benefit indicators, including carbon reduction, pollution reduction, resource comprehensive utilisation, and green expansion indicators, alongside the qualitative indicator description of environmental benefit of the project for green projects funded by green financial products, distinguishing between mandatory and recommended indicators. This establishes a foundation for the measurability, reportability, and verifiability of environmental benefits in green finance, facilitating application by market participants.

The General Office of CBIRC and the General Office of PBoC jointly issued the Implementation Plan for High-Quality Development of Green Finance in the Banking and Insurance Sectors.[24] This document explicitly requires banking and insurance institutions to progressively establish and improve information disclosure mechanisms. Financial institutions’ environmental information disclosure remains in its early stages. Moving forward, all market participants must jointly promote the widespread adoption of green bond environmental disclosure standards to advance the standardisation of environmental benefit disclosure in green finance. This collective effort will contribute to building a Beautiful China and creating a brighter future.

For listed companies, following the release of the Guidelines for Corporate Sustainability Disclosure for Listed Companies by the Shanghai Stock Exchange, Shenzhen Stock Exchange, and Beijing Stock Exchange in 2024, the three major exchanges jointly issued the Guidelines for Preparing Sustainable Development Reports for Listed Companies on January 17, 2025.[25] The first batch of guidelines includes two specific documents: “General Requirements and Disclosure Framework” and “Addressing Climate Change.” The former establishes a four-element disclosure framework — “governance, strategy, impact, risk, and opportunity management, indicators and targets” — along with methodologies for identifying material issues. The latter elaborates in six sections on assessment methods for dual materiality (impact materiality and financial materiality), climate adaptation analysis, mandatory Scope 1 and Scope 2 accounting, and Scope 3 voluntary phased disclosure. It specifies 22 specific climate-related disclosure points, addressing key challenges and current practices faced by listed companies to provide detailed operational guidance.

As one of the world’s first exchanges to strengthen climate-related disclosure requirements to align with IFRS S2, the Hong Kong Exchanges and Clearing Limited (HKEX) implemented a new set of climate-related disclosure rules effective January 1, 2025. The new climate provisions are being incorporated into the new Part D of the Environmental, Social and Governance Reporting Guidelines (ESG Guidelines) under the Rules Governing the Listing of Securities of The Stock Exchange of Hong Kong Limited. This initiative will significantly enhance the transparency and comparability of climate-related disclosures by listed companies, positioning Hong Kong at the forefront of sustainable finance and marking a significant step forward in establishing a comprehensive climate reporting framework.

Table 2: Key trends in disclosure policy standards

| Positive progress | Challenges |

| Stricter and more standardised climate and sustainability reporting guidelines for listed and non-listed companies;Alignment with international reporting standards (IFRS) in Hong Kong and efforts to harmonise the mainland financial system; Voluntary scope 3 disclosure. | Lack of broader sustainability disclosure standards (e.g., social impacts) Lack of disclosure policies in emerging areas such as green insurance and biodiversity finance;Corporate sustainability disclosure remains voluntary, with uneven compliance levels;In practice, companies often omit Scope 3 emissions disclosure;Insufficient data and professional disclosure capabilities, and a lack of specific policy support and guidance. |

2.3 Incentive and restraint mechanisms

The incentive and restraint mechanisms of green finance provide clear behavioural guidance for entities and financial institutions through policy steering and institutional arrangements, aiming to direct funds toward green sectors and curb high-carbon economic activities. In 2025, China’s development in this area has been characterised by simultaneous central coordination and local innovation, continuing a tradition of building a multi-level and systematic policy framework.

At the central level, the institutional design featuring parallel incentive and restraint tracks has become increasingly clear. In January, the NFRA and PBoC jointly issued the Implementation Plan for High-Quality Development of Green Finance in the Banking and Insurance Sectors, marking a move towards a more refined and institutionalised incentive-constraint mechanism for green finance.[26] The plan not only requires financial institutions to establish internal green finance assessment and incentive mechanisms, but also encourages resource allocation through measures such as preferential internal transfer pricing and dedicated credit quotas. On the constraint side, it explicitly incorporates ESG assessments into credit and underwriting decisions, controls credit for projects with high energy consumption, high emissions, and low standards, aiming to prevent greenwashing and disorderly competition in green finance at the source. This plan can be regarded as a significant attempt to build a closed-loop incentive-constraint mechanism at the institutional level.

Building on this, macro-level policies have further strengthened overall support for green finance. The Government Work Report 2025, released by the State Council in March, explicitly proposes increasing fiscal policy support for green energy and ecological governance,[27] including issuing new ultra-long-term special treasury bonds and local government special bonds to reduce the financing costs of green projects. This reflects the coordinated efforts of fiscal and monetary policies, seeking to stimulate green investment vitality from the financing cost side.

Subsequently, the Recommendations of the Central Committee of the Chinese Communist Party (CCP) on Formulating the 15th Five-Year Plan for National Economic and Social Development, released in October, further elevated the policy system for green and low-carbon development.[28] The document emphasises improving the synergy of fiscal, financial, and pricing policies and, for the first time, systematically proposes establishing long-term mechanisms for green consumption incentives and ecological compensation to guide sustained social capital flow into green industries. Regarding constraints, the recommendations propose implementing a dual-control system for total carbon emissions and intensity, promoting carbon management at the local, industry, and enterprise levels, and driving green transformation in key areas such as industry and urban-rural development.

At the local level, various financial institutions have carried out product and service innovations based on regional characteristics, such as:

- Industrial Bank Urumqi Branch designed a comprehensive service scheme of “water abstraction rights pledge + traditional collateral pledge”, successfully issuing Xinjiang’s first green mine water abstraction rights pledged loan of RMB 200 million (USD 28.6 million) to support the construction of a mine water recycling system.[29] This case reflects an innovative path combining green finance with resource rights pledging, providing a financial solution for realising the value of ecological resources.

- Tianjin Binhai Rural Commercial Bank issued a RMB 50 million (USD 7.15 million) dual-certification loan of “transition finance + carbon footprint”. By establishing a tracking period and a third-party evaluation mechanism, it links financing costs to corporate carbon reduction performance.[30] This dynamic incentive-constraint mechanism not only reduces corporate transition financing costs but also helps prevent fund mismatch and transition deviation risks, embodying the “process management” characteristic of transition finance.

- Bank of Jiangsu Suzhou Branch issued a RMB 193 million (USD 27.6 million) green loan. This product was simultaneously included under the dual categories of “biomass energy utilisation” and “air pollution control and treatment” in the Biodiversity Finance Catalogue (Trial Version),[31] becoming the nation’s first green credit product with an “ecological dual-label”. This move demonstrates the financial sector’s exploratory integration in synergistically advancing the “dual-carbon” goals, pollution prevention, and biodiversity protection, expanding the connotative boundaries of green finance.

These local practices indicate that the incentive-constraint mechanism relies not only on the central policy framework but also requires local financial innovation and scenario-based application to be effectively implemented, forming a pattern of positive interaction between central and local levels and coordinated advancement of policies and products.

Table 3: Relevant trends in incentive and restraint mechanisms

| Positive progress | Challenges |

| Broad government support from many ministries on green incentives and restraints;Broad political support from CCP to strengthen the green transition including green finance; Stronger coordination of fiscal and monetary policies to reduce green project financing costs;Local innovation in green financial products, forming diverse practical cases. | Insufficient transition finance incentive tools to replace expiring short-term monetary instruments;Poor inter-departmental policy coordination, difficulty in matching returns and risks of green projects. |

2.4 Green financial products and market system

In 2025, China has advanced its green finance products and market system in areas such as green bonds, transition bonds, carbon footprint accounting, emission trading, and green electricity certificates, gradually building a multi-level, market-oriented, and internationally aligned green financial product system.

2.4.1 Green and transition bonds

Significant progress has been made in the institutional optimisation and opening up of the green bond market. In February, NAFMII issued a notice further optimising the mechanism for overseas institutions to issue green bonds in the interbank bond market. It clarifies that green project identification can be based on domestic catalogues,[32] promoting international standard alignment and issuance facilitation. During the same period, MoF issued the Green Sovereign Bond Framework of the People’s Republic of China,[33] aiming to explore the issuance of green sovereign bonds overseas, attract international funds to support domestic green and low-carbon development, and contribute to advancing green finance (China issued its first sovereign green RMB in London later that year).

In February 2025, NFRA and PBoC issued the Implementation Plan for High-Quality Development of Green Finance in the Banking and Insurance Sectors. This plan aims to shift green loan development from a focus on scale to “high-quality expansion” under unified standards, refined management of loan allocation and stronger climate risk constraints.[34] Within this policy framework, green insurance is positioned as a core pillar of green finance. It plays a dual role by providing risk protection on the liability side and supplying long-term green capital on the asset side, thereby linking risk mitigation with the financing needs of green and low-carbon development. On the product side, the plan calls for improving the green insurance product system and refining catastrophe and environmental liability insurance. It also encourages the development of carbon-related products, such as carbon sink price insurance and carbon emissions trading insurance, to provide lifecycle risk coverage for industrial upgrading, energy transition, pollution control and the development of carbon markets.

To further unify the standard system, in June 2025, PBoC, NFRA, and CSRC jointly issued the Green Finance Supported Project Directory (2025 Version).[35] As a major upgrade of the green finance standard system, this directory achieves the unification of identification standards for various green financial products, helping to address the risks of “greenwashing” and market fragmentation caused by inconsistent standards in the past.

2.4.2 Carbon footprint quantification

Carbon footprint quantification is a key foundation for green finance to move from the “project level” to the “product and supply chain level”. Since 2025, China has accelerated its layout in carbon footprint accounting standards, certification systems, and information disclosure, with a preliminary system taking shape.

Regarding accounting standards, MEE led efforts with other departments to jointly issue the Guidelines for Developing Product Carbon Footprint Accounting Standards in January 2025.[36] The Guidelines unify core requirements such as accounting boundaries and data acquisition, aiming to establish a unified and standardised accounting standard system. Subsequently, the Certification and Accreditation Administration of the People’s Republic of China (CNCA) released certification implementation rules in March, standardising the entire process of carbon footprint label certification and providing an operational basis for enterprises.[37] In June, the MEE released a progress report on system construction, systematically summarising phased achievements in standards, certification, and information disclosure.[38]

Overall, China’s carbon footprint management has strengthened a closed-loop framework of “standards—certification—disclosure”. However, issues such as a lack of industry-specific standards and weak accounting capabilities of small and medium-sized enterprises still constrain its widespread application.

2.4.3 Emission Trading System (ETS) and China Certified Emission Reduction Credits (CCER)

The national carbon market has continued to deepen in terms of coverage, trading mechanisms, and institutional development. In March, MEE issued a plan to include three high-energy-consuming industries—steel, cement, and aluminium smelting—into the national ETS.[39] This significantly increased the number of covered enterprises and the scale of carbon emissions, accompanied by the release of multiple technical specifications, promoting the deepening of the carbon market into industries and the refinement of its institutions.

Importantly, in 2025, the Opinions on Promoting Green and Low-Carbon Transformation and Strengthening the National Carbon Market explicitly state that the core of quota management will gradually shift from intensity control to total volume control.[40] By 2027, total volume control will be prioritised for industries with stable carbon emissions. By 2030, a carbon market based on total volume control will be established. Concurrently, a combination of free and paid quota allocation will be implemented, and a quota reserve mechanism will be established to ensure a smooth transition and enhance market stability.

The National Carbon Market Development Report (2025), released in September, shows that the annual trading volume of the ETS reached a record high, with a compliance rate close to 100%, indicating overall stable and orderly market operation.[41] The CCER market has developed steadily since its relaunch in 2024, with methodologies expanded to six, and the number of registered projects and trading volume gradually increased. The average transaction price repeatedly exceeded 100 RMB/ton, demonstrating that the voluntary emission reduction market is forming effective price signals and incentive mechanisms. The coordinated development of the carbon market and CCER provides market-based pricing tools and flexible compliance channels for the low-carbon transition of the economy and society.

2.4.4 Green Electricity Certificates (GECs)

Breakthroughs have been made in the institutional design and cross-domain linkage of the green electricity certificate market. In March, NDRC and other departments issued Opinions on Promoting the High-Quality Development of the GEC Market,[42] clarifying phased targets and taking simultaneous actions from both the supply and demand sides. On the supply side, efficient issuance and cross-provincial circulation mechanisms were established. On the demand side, green electricity consumption proportion requirements were set for key industries, pushing the GEC market from a “voluntary” model towards a “combination of mandatory and voluntary” one.

Notably, in October, MOFCOM incorporated GECs into the green trade support system, supporting the increase of green electricity penetration in foreign trade industrial chains and promoting international recognition of China’s GEC system.[43] This move signifies that the function of GECs has extended from an energy and environmental policy tool to a trade policy tool for addressing international green trade barriers and enhancing the green competitiveness of foreign trade, highlighting its cross-sectoral synergistic value.

Table 4: Recent trends in product and market systems

| Positive progress | Challenges |

| Optimisation of green bond mechanisms and facilitation of overseas issuance;Unification of the Green Finance Supported Project Directory, enhancing standard consistency;Unification of carbon footprint accounting standards and implementation of certification rules;Expansion of ETS to industries like steel, growth in CCER trading after restart;Ambition to move to a cap and trade system in ETS (rather than an intensity-based system);Establishment of cross-provincial circulation mechanisms for GECs and linkage with green trade. | Gaps in industry-specific carbon footprint standards, weak accounting capabilities of SMEs;Imperfect GEC price mechanism, barriers to international mutual recognition. |

2.5 International cooperation and standards

In 2025, China’s government and private financial institutions continued international cooperation in green finance policy and thought leadership. This also includes the expansion of the Multi-jurisdictional Common Ground Taxonomy (see above).

In regional and multilateral standard integration, China-Singapore cooperation has emerged as a key driver. On July 10, 2025, the third meeting of the China-Singapore Green Finance Working Group was successfully held.[44]The agenda directly addressed core challenges and opportunities in policy cooperation, focusing on three key areas: interoperability of sustainable finance standards between the two countries, innovation in green and transition finance products, and leveraging technology to advance green finance and carbon market development. China stated that beyond advancing the agendas of existing working groups, China-Singapore green finance cooperation could further extend to ASEAN, exploring financial solutions to support its green and sustainable development. This reflects China’s approach of leveraging bilateral initiatives to drive multilateral expansion in green finance policy.

In June, the IFRS Foundation hosted the Beijing International Sustainability Conference in cooperation with international partners to discuss best practices and the role of the ISSB standards. In building a robust sustainability-disclosure ecosystem.[45] China also continued its support for ISSB standard development, particularly around Scope 3 disclosures.

Other noteworthy examples include the 11th China-UK Economic and Financial Dialogue, which was held in Beijing in January. Regarding green finance, both sides reaffirmed their status as partners in this field and agreed to establish new working groups in areas such as sustainable disclosure, transition finance, and biodiversity finance.[46] To implement this high-level consensus, the Seventh China-UK Green Finance Working Group Meeting convened in London in June, focusing on practical topics including transition finance, nature and biodiversity finance, the Belt and Road Green Investment Principles (GIP), sustainable disclosure, and carbon markets.[47]

Meanwhile, China and France maintained close coordination on macro-policy aspects of climate finance. On the tenth anniversary of the Paris Agreement, the two sides issued a joint statement on climate change, reaffirming their firm commitment to limiting global warming to 1.5°C and upholding the multilateral system centred on the Paris Agreement.[48]

Table 5: Trends in international green finance

| Positive progress | Challenges |

| Strengthened common ground taxonomy work; Established institutionalised cooperation with the UK and Singapore, forming a dedicated green finance working group;Deepened China-France climate finance coordination, reaffirming commitments under the Paris Agreement. | Chinese financial institutions have limited participation in voluntary international associations and standard-setting bodies such as GFANZ and TNFD;Differences in international standards across multiple areas—including sustainable disclosure, transition finance, and biodiversity finance—hinder cross-border project collaboration. |

3. Green finance in China in practice

Green finance application in China has grown in 2025, with the focus gradually shifting from an emphasis on “quantity” to an emphasis on “quality.” As such, green finance continues to play its role as one of the five major tasks in advancing the dual-carbon targets of carbon peaking by 2030 and climate neutrality by 2060.

In this section, we provide a detailed review of the development of green finance across different types of financial instruments in 2025.

- Green loans

- Green bonds

- Common Ground Taxonomy Bonds

- Panda bonds

- Special Green bonds

- Transition bonds

- Green insurance

- Green funds

3.1 Green loans under the new classification

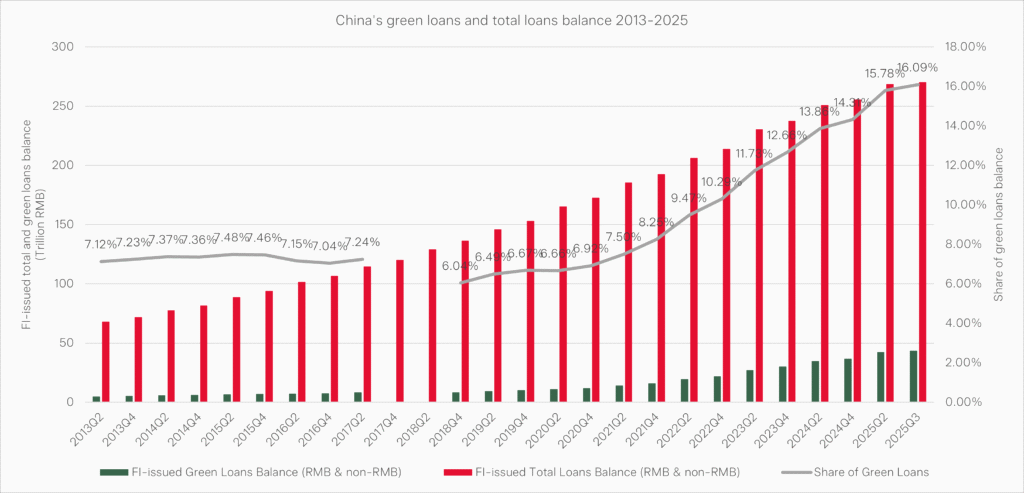

By the end of Q3 of 2025, the outstanding balance of RMB- and foreign-currency green loans reached RMB 43.51 trillion (USD 6.2 trillion), up 6.47 trillion (USD 0.9 trillion), or 17.5% from the beginning of the year. Green loan growth outpaced the growth of other loans.[49] However, it should be noted that the 2025 figures are not directly comparable with earlier data on green loan balances, as the statistical coverage and eligibility criteria were revised at the beginning of 2025. Under the pre-2025 framework (see Table 6), green-loan balances rose by 18.9% from the beginning of 2024 to end-Q3 2024, compared with 32.3% over the same period in 2023. The share of outstanding green loans in total lending increased to 16.09% by Q3 2025, from 15.78% in the beginning of 2025 (see Figure 1).

Table 6: Comparison between green loan identification frameworks

| Green Industry Guidance Catalogue (2019 Edition) | Green Finance Supported Project Catalogue (2025 Edition) | |

| Positioning & applicability | Primarily an industrial catalogue that classifies “green” activities by industrial sectors and project types | Primarily a financial identification standard applicable across green financial products (e.g., green loans and green bonds). |

| Coverage | Six major sectors: energy-saving & environmental protection; clean production; clean energy; ecological environment; green upgrading of infrastructure; and green services. | Nine domains: energy saving & carbon reduction; environmental protection; resource recycling; low-carbon energy transition; ecological protection, restoration and utilisation; green upgrading of infrastructure; green services; green trade; and green consumption. |

| Identification logic | Functions largely as an activity list and is not designed specifically for financial statistics, so implementation often relies on interpretation and mapping. | Designed as a verifiable identification framework: item-level, tabular criteria with explicit industry codes, item names, eligibility conditions/standards, and notes, and includes fields such as “contribution to GHG emission reduction,” improving consistency and auditability. |

| Positioning & applicability | Primarily an industrial catalogue that classifies “green” activities by industrial sectors and project types | Primarily a financial identification standard applicable across green financial products (e.g., green loans and green bonds). |

Source: authors compiled based on published information.

Figure 1: China’s green loans and total loans balance 2013-2025

Under the new 2025 classification system, the use of green loans is grouped into three categories: green upgrading of infrastructure, green-oriented transition of energy, and ecological conservation, restoration and utilisation. By sector, the green loan balance for transportation, warehousing, and postal industries reached RMB 7.91 trillion (USD 1.1 trillion), whereas the balance for the production and supply of electricity, gas and water stood at RMB 8.74 trillion (USD 1.2 trillion) (see Figure 2).

Figure 2: Green loans balance by usage 2018-2025

Source: authors’ calculations based on PBoC public reports; sample includes 21 major banks.

3.2 Green bonds[50]

China’s onshore green bond market has seen multiple phases of growth and decline since 2016: Between 2018 and 2022, annual green bond issuance rose rapidly, but momentum weakened in 2023 and then fell markedly in 2024, with issuance volume down 31.62% year-on-year (YoY).

By the end of 2025, the slowdown reversed and issuance rebounded by 56.5% compared to the year ended 2024 to RMB 1.09 trillion (USD 154.72 billion). The annual number of green bond issues broadly followed the same trajectory, falling 13.75% YoY in 2024 before rebounding in 2025, rising 24.42% relative to the year ended 2024. Even so, yearly issuance has not yet returned to the historical peak reached in 2022. At the same time, bond repayments climbed to a record RMB 772.19 billion (USD 109.53 billion), resulting in net green bond financing of RMB 318.59 billion (USD 45.19 billion) in 2025. Although this exceeded the net financing achieved in 2024, it remained significantly below the levels seen in 2022 and 2023 (see Figure 3).

Figure 3: Re-acceleration of China’s onshore green bond issuance

Medium-term green bonds (with maturities of 1–5 years) have consistently dominated onshore green bond issuance. Since 2021, the share of short-term bonds (≤1 year) has increased, suggesting that issuers have increasingly used the bond market to meet short- to medium-term financing needs (see Figure 4).

Figure 4: Maturity distribution of onshore green bonds issuance

By December 8, 2025, the proceeds of onshore green bonds in China were mainly allocated to three areas: around 27% supported the green and low-carbon transition of energy, 25% financed green upgrading of infrastructure, and 22% flowed into the energy-saving and environmental protection industry (see Figure 5).

Figure 5: Shares by use of proceeds in 2025

Main issuers in the Chinese onshore green bonds market continue to be state-owned enterprises (SOEs), accounting for 84.53% of total green bond issuance volume in 2025 (similar to the 86.75% in 2024). Private-sector issuers remained a distant second, while issuance by provincial governments has been declining since 2023 from RMB 267 billion (99 bonds) to RMB 4.08 billion (5 bonds) in 2025 (see Figure 6).

Figure 6: China’s onshore green bond issuance by ownership

Apart from onshore green bonds, Chinese issuers tapped international markets with offshore green bond issuances worth RMB 15.96 billion (USD 2.3 billion) across 23 deals by December 3, 2025. The issuers are mainly Chinese financial institutions and “high-quality corporates”,[51] with proceeds primarily allocated to wind power, transportation and other clean energy-related sectors. China also debuted its first global green sovereign bond in April 2025, issuing RMB 6 billion (USD 0.85 billion) with a coupon rate below 2%[52] on the London Stock Exchange.[53]

In comparison to international markets, China’s green bond market growth bucks the trend of falling global green bond issuances: as of late October 2025, the total global issuance of green bonds had fallen by 11% YoY to USD 506 billion (RMB 3.5 trillion), according to a report by China Energy News, citing data from London Stock Exchange Group (LSEG). Due to China’s growth, China accounted for 20% of global green bond issuances, making China the world’s largest green bond market.[54]

Despite their growth, green bonds still account for a relatively small share of the total bond volume of the onshore bond market. By the end of December 2025, annual issuance of onshore green bonds was equivalent to 1.22% of the issuance of onshore total bond, up from 0.87% in 2024.

3.3 Common Ground Taxonomy (CGT) Bonds

The EU–China Common Ground Taxonomy (CGT) provides an internationally aligned standard for labelling green bonds. Issuance volume in the first eleven months declined slightly in 2025 compared with the same period in 2024, even as a growing number of CGT-aligned green bonds were issued in China’s interbank green bond market (see Figure 7). By the end of November 2025, 292 out of 503 CGT-labelled green bonds remained outstanding. These 292 bonds accounted for 25.1% of the total number of outstanding green bonds in China’s interbank market. They also totalled RMB 334.20 billion (USD 47.4 billion) in outstanding volume, representing 16.2% of the China total outstanding interbank green bond volume.[55]

The top three activity categories by use of proceeds for CGT bonds were wind power generation (25.1%), construction and operation of urban and rural public transport systems (23.1%), and hydropower generation (19.2%).[56]

Figure 7: Monthly issuance of China-EU CGT-aligned green bonds in China

Source: authors based on Green Finance Committee (GFC) data.

3.4 Panda Bonds

Panda bonds (bonds issued by non-Chinese entities in RMB on China’s domestic bond market) remain attractive to international investors in 2025. By the end of December 2025, the issuance amount totalled RMB 183.56 billion (USD 26.04 billion), in line with the RMB 194.80 billion (USD 27.63 billion) issued in all of 2024 (see Figure 8).

Against a backdrop of relatively lower interest rates within China with spillovers to onshore RMB bond issuances, Panda bond issuers were often able to secure funding at more favourable costs compared to other major markets.

Figure 8: Panda bond issuance

According to Fareast Credit’s H1 2025 report, issuance of sustainability-themed Panda bonds totalled RMB 26.8 billion (USD 3.8 billion) by the first half of 2025, a 33.98% decline compared to the first half of 2024. Sustainability-themed Panda bonds accounted for 7.18% of total Panda bond issuance in the H1 2025, 2.16% lower than in H1 2024.[57]

3.5 Special Green Bonds (Carbon, Water, Blue)

By the end of December 2025, the total issuance of carbon-neutral bonds, a special type of green bonds regulated by NAFMII,[58] reached RMB 150.16 billion (USD 21.30 billion) across 214 bonds. By the end of 2024, 193 bonds had been issued, totalling RMB 180.26 billion (USD 25.6 billion). In line with the decline in carbon-neutral issuance, the issuance of water environmental protection bonds and blue bonds also fell in 2025 (see Figure 9).

Figure 9: Special green bonds issuance

Source: authors based on Wind data.

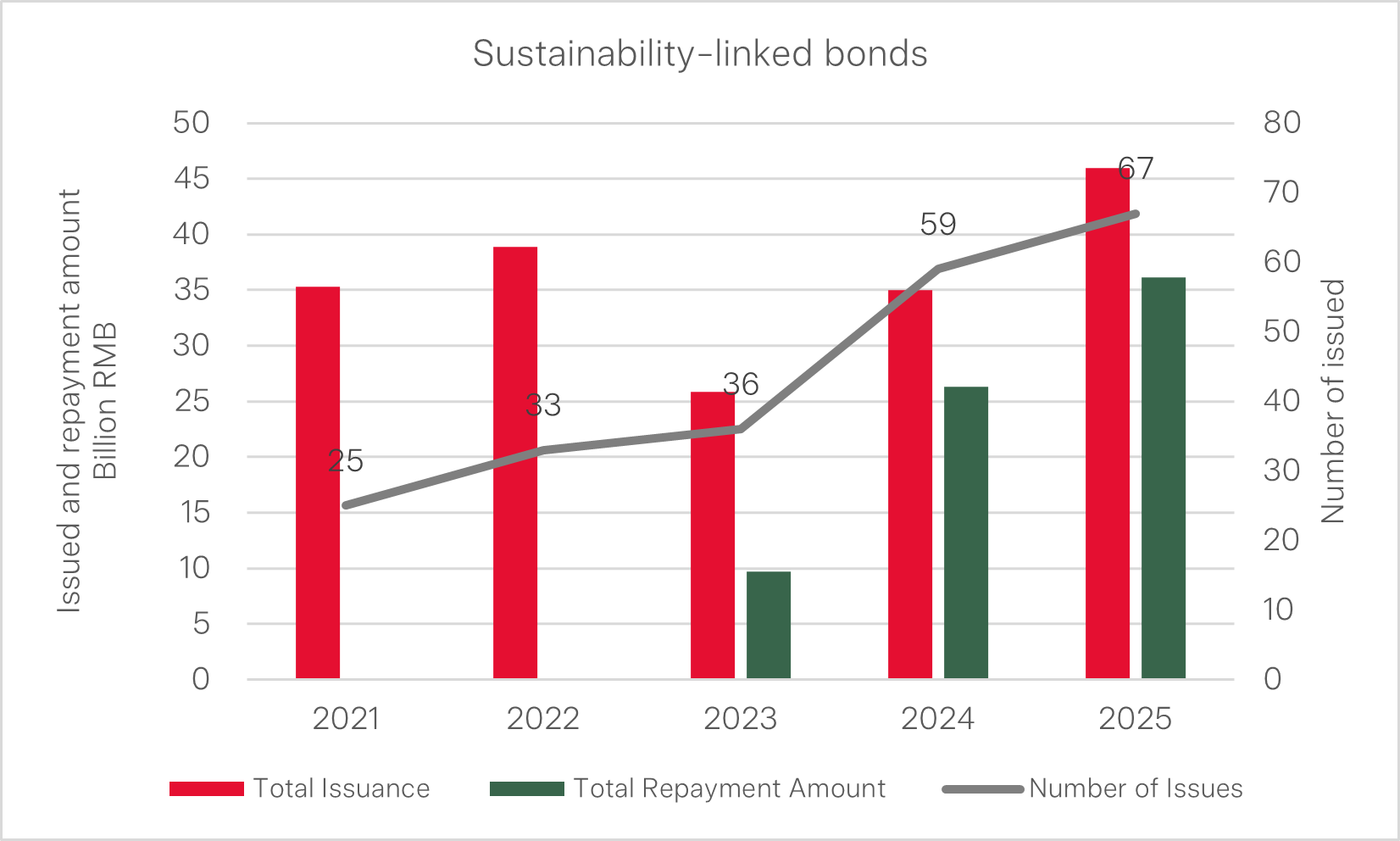

3.6 Transition bonds

According to the China Transition Bond White Paper 2025 published by China Central Depository & Clearing (CCDC),[59] transition bonds can be classified into linked transition bonds (including sustainability-linked bonds and low-carbon transition-linked bonds that are linked to ex-post evaluation of sustainability outcomes) and non-linked transition bonds (using, e.g., a taxonomy for ex-ante definition of transition activities). In China, transition bonds have increasingly tilted towards linked instruments: Between 2021 and 2024, the cumulative issuance volume of linked transition bonds was nine times that of non-linked transition bonds, indicating a clear market preference for linked structures.[60]

Market dynamics in 2025 further reflect this pattern. By the end of December 2025, both sustainability-linked bonds (SLBs) and low-carbon transition-linked bonds recorded increases in new issuance volume; however, a high level of repayments has led to a gradual decline in net financing over time. By contrast, transition bonds have seen a fall in total issuance volume even as the number of bonds issued has continued to rise (see Figure 10).

Figure 10: Stability-linked bonds

Source: authors based on Wind data.

Transition bonds have primarily supported the decarbonisation of high-emitting sectors rather than already “green” activities. Transition-related bonds have effectively created a funding pool for high-carbon industries: approximately RMB 13.93 billion (USD 1.9 billion). Between 2021 and 2024, the top three recipient industries were: energy-saving and carbon-reduction retrofits; energy-efficiency upgrades, energy-saving and carbon-reduction retrofits of coal-fired power units; and clean and efficient utilisation of coal. Together, these three areas attracted approximately RMB 13.93 billion (USD 1.9 billion), representing 85.55% of total transition-related bond financing.[61]

3.7 Green insurance: from policy guidance to detailed implementation

By the end of 2024, premium income from green insurance nationwide had reached RMB 333.1 billion (USD 47.2 billion), providing risk coverage in excess of RMB 330 trillion (USD 46.8 trillion).[62] In the first half of 2025, the People’s Insurance Company of China (PICC) reported that its green insurance business provided risk coverage totalling RMB 131.6 trillion (USD 18.6 trillion), a YoY increase of 16.3%.[63] Over the same period, direct premium income from green insurance business at Ping An Insurance reached RMB 36.84 billion (USD 5.2 billion), a YoY increase of 51.8%.[64] These figures indicate that within a short period, green insurance has moved from a niche segment to a key component of the financial system’s support for the green transition.

3.8 Green funds offer competitive returns alongside environmental benefits

After a rebound in 2024, new issuance activity in the green fund[65] segment slowed by the end of December 2025, primarily due to a contraction in new equity and bond fund launches (see Figure 11). Equity fund issuance fell from 189.26 billion shares in 2024 to 51.56 billion shares in 2025, a 72.76% decline, the sharpest drop among all fund categories. In contrast, hybrid funds increased by 22.07 billion shares in 2025, reaching 25.38 billion shares.

According to the China ESG Fund Development Report 2025 published by Sino-Securities Index Information Service, as of 30 June 2025, China’s ESG fund market continued to expand, comprising 372 ESG funds with total assets under management (AUM) of RMB 301.38 billion (USD 42.7 billion). Among these, 298 are actively managed funds with AUM of RMB 283.60 billion (USD 40.2 billion), significantly outweighing the 74 passive funds, which have AUM of RMB 17.78 billion (USD 2.5 billion).[66]

Figure 11: China’s green funds issuance 2016-2025

Source: authors based on Wind data[67].

Largest off-exchange ESG-themed index product in the domestic public fund industry: According to ChengTong, on 26 August 2025, the Rongtong CSI ChengTong Central SOEs ESG ETF Feeder Fund was launched with an initial offering size of RMB 960 million (USD 136.1 million), which, according to Wind, represents the largest first-offering scale for an off-exchange ESG-themed index product in the history of China’s public fund industry.[68]

The majority of ESG funds deliver high returns: According to China Securities Journal, Wind data show that, as of 19 September 2025, among 107 ESG-themed funds (classified by Wind as “pure ESG theme” funds), around 87% had achieved positive year-to-date returns. The best-performing fund recorded a gain of over 65%, and more than 20 ESG-themed funds delivered returns above 30%, indicating that ESG products have, in many cases, combined responsible investment objectives with attractive financial performance.

4. Green finance trends for 2026 and beyond

While 2025 can be viewed as a year of alignment and consolidation for China’s green finance framework, this section identifies seven trends that are likely to shape China’s green finance landscape in the future.

1. Acceleration of transition finance as a key bridge between “pure green” and high-carbon asset phase-out based on catalogues

While the relevance of transition finance has grown since 2022 (including the 2025 release of transition finance standards for sectors such as steel, coal power, building materials and agriculture), this will be a core focus going forward. Drafting of standards for an additional seven sectors, including petrochemicals, chemicals, shipping and non-ferrous metals, is underway.[69]

The challenge will be to balance risks of rapid transition on asset values and jobs, with the need to rapidly decarbonise to meet the “30-60” carbon goals and reduce de facto climate risks. A further challenge will be developing realistic transition standards that address current concerns while also spurring investment in future (uncertain) technology developments (such as green metals, green construction, green agriculture). Over the coming years, transition finance is therefore likely to grow into a core complement to “pure green” finance, especially for carbon-intensive industries.

2. Emphasis on climate-related disclosure, including data and control

In 2025, China issued Corporate Sustainability Disclosure Standard No. 1: Climate (Trial),[70] taking a concrete step toward a domestic sustainability disclosure regime with climate at its centre. Larger listed companies and financial institutions are expected to pilot more structured climate-related disclosures aligned with international practice, while stock exchanges refine ESG and sustainability reporting guidelines for issuers. For labelled green and sustainability bonds, regulators are tightening expectations on use-of-proceeds, impact indicators and external review.

However, to meet disclosure requirements, capacity for data and internal controls will be strengthened. The use of big data to prepare and validate disclosure statements will be expanded with significant investment opportunities for data providers and verifiers. A big risk remains greenwashing, with AI playing both an exacerbating role (in creating misleading reports) and a controlling role (for oversight).

3. Banking and insurance shift from product-level green offerings to portfolio-level transition strategies

The Implementation Plan for High-Quality Development of Green Finance in the Banking and Insurance Sectors[71] explicitly positions green finance as a core pillar of the banking and insurance business. It calls for a higher share of green activities in total assets, stronger climate and environmental risk management, and reinforced support for energy transition, industrial upgrading and pollution control. In practice, this implies a shift from isolated “green credit products” toward portfolio-level targets, differentiated treatment of high- and low-carbon assets, and tighter links between underwriting, investment and ESG performance. Green and transition finance are likely to be increasingly embedded in institutions’ capital planning, internal pricing and incentive systems, rather than treated as add-ons.

4. Biodiversity and blue finance move from concept to standardised, scalable products

Chinese regulators in 2025 initiated pilot biodiversity finance project catalogues across multiple provinces and municipalities, focusing on nature-based solutions, ecological restoration and ecosystem services. The intention is to bring biodiversity-related activities into a framework that can be linked to loans, bonds and insurance products. At the same time, coastal regions and sectoral regulators are exploring standards and pilots for blue finance, targeting marine ecosystem protection, coastal resilience and sustainable ocean-related industries. Biodiversity- and ocean-linked financing instruments are likely to shift from ad-hoc innovations to more templated, replicable products that can be scaled via mainstream financial institutions.

5. Digital and AI-enabled infrastructure underpins “precision” green and transition finance

The policies in 2025 create a stronger foundation for digitalising green finance data and workflows.[72] Leading banks, insurers and pilot zones are already experimenting with big-data platforms, distributed ledgers and AI models to improve project screening, real-time emissions tracking and scenario analysis. These tools are being linked to carbon-accounting systems, collateral registries and ESG risk-management frameworks, with the aim of lowering transaction costs and improving risk-pricing accuracy.

6. China to set green finance standards in Global South – and North

With the withdrawal of major economies (such as the US) and the withdrawal of private institutions from setting green finance standards, China will be looked up to as a standard setter. As the self-styled “largest developing country”, China aims to be a role model for green finance cooperation in the Global South, but without Western leadership, China will increasingly be seen as the global leader and standard setter based on its vast experience with green finance standards and implementation.

This does not mean that international collaboration on green finance (e.g., through ISSB) will be determined by China, but that China’s institutions have a stronger say in the direction of standard-setting.

7. Green finance becomes a key lever in climate diplomacy and South–South cooperation

China is increasingly presenting its domestic green finance reforms as part of its contribution to global climate and biodiversity goals and as a basis for deeper South–South cooperation.[73] Official narratives around green finance emphasise consistency with the Paris Agreement and the Kunming–Montreal Global Biodiversity Framework, while reiterating principles such as “common but differentiated responsibilities” and respect for national circumstances. Green and transition finance are being woven into bilateral and multilateral initiatives, including green development funds, co-financing with multilateral development banks and taxonomy cooperation. In the future, China is likely to further link its taxonomy, disclosure system and transition finance standards with its positions in global climate negotiations, using green finance both as a domestic policy tool and as an external signalling device.

5. Recommended actions to accelerate green finance in China

Green finance in China saw significant developments in 2025 in support of its carbon peak (2030) and climate neutrality (2060) goals. Notable policy improvements were made in areas such as standard unification, product innovation, and mutual recognition of standards.

To further improve China’s green financial system, we see opportunities in addressing the following challenges:

1. Implement a national transition finance system

The first batch of transition standards for high-emission industries remains in the pilot phase, while the second batch of industry standards has yet to be finalised. Although transition finance standards for four high-carbon sectors—steel, coal power, building materials, and agriculture—have been piloted in some provinces and cities, unified national standards for transition finance have not been issued. This leads to fragmented local standards and inconsistent project identification criteria, leaving financial institutions without a unified basis for project evaluation, risk pricing, and capital allocation, thereby increasing the risk of “transition-washing”.

A transition finance framework should clearly define eligibility criteria for transition activities, requirements for corporate transition plans, disclosure standards, and corresponding incentive and restraint mechanisms. At the same time, transition finance standards should be effectively aligned with the Green Finance Support Project Catalogue (2025 Edition), providing financial institutions with a clear and operational policy basis and reducing the risk of transition-washing.

2. Strengthen environmental information disclosure quality and data foundations

Enterprises and financial institutions exhibit significant shortcomings in ESG and climate-related disclosures capacity. Fragmented content, inconsistent standards, poor data comparability, missing climate risk data, and inconsistent carbon accounting methods make it difficult for investors to accurately assess the authenticity and environmental benefits of green assets. Furthermore, SMEs’ limited disclosure capacity and willingness to disclose exacerbate information asymmetry, hindering targeted green finance allocation and risk pricing.

To strengthen disclosure quality, relevant authorities should strengthen sectoral application of carbon footprint management systems that go beyond a one-size-fits-all approach, but focuses on materiality. The standards should be fully harmonized with international standards, such as IFRS. At the same time, the development of public carbon footprint accounting service platforms for small and medium-sized enterprises (SMEs) should be accelerated to reduce compliance costs. Product-level carbon footprint performance should be progressively incorporated into the assessment frameworks for green credit and green bonds, thereby reinforcing financial incentives for emissions reduction across the full life cycle.

3. Expand the carbon market: China should accelerate the expansion of the national carbon market and improve carbon price formation mechanisms

Building on the inclusion of the steel, cement, and aluminium smelting sectors, a clear roadmap should be established for incorporating additional high-emitting industries such as chemicals, paper, and aviation, with the aim of gradually covering major emission sources. Carbon allowance management should shift from intensity-based control toward absolute caps, supported by allowance reserve and price stabilisation mechanisms to enhance the reliability and stability of carbon price signals.

4. Expand the green capital market through issuer diversification.

China’s green finance products and markets primarily consist of green loans. Green bonds are important but still lag in volume and issuer diversity (most are issued by SOEs) and often have short tenors.

Broader market development requires diversification of issuers and products, and green finance innovation remains insufficient beyond initiatives confined to pilot stages. Duplication or overlaps between green finance products further increase the risk of investor and issuer confusion (e.g., green bonds, climate bonds, low-carbon bonds).

Building on the Green Sovereign Bond Framework of the People’s Republic of China, China should actively promote the issuance of green sovereign bonds, leveraging sovereign credit to play a guiding and demonstration role. This would help attract long-term international capital into China’s green and low-carbon sectors and, through a signalling effect, encourage local governments and corporate issuers to expand green bond issuance, thereby enhancing China’s influence within the global green finance system.

Efforts should also be made to improve liquidity in the green bond market and strengthen its long-term financing function. In response to the slowdown in primary issuance and insufficient activity in secondary markets, market-based mechanisms should be enhanced by introducing green bond market-making arrangements and improving repo and collateral frameworks to deepen market liquidity among private issuers. In parallel, increasing the supply of medium- and long-term green bonds would better match the financing needs of clean energy and green infrastructure projects and attract long-term institutional investors such as insurers and pension funds.

5. Enhance central bank support: A multi-tiered and long-term incentive and restraint mechanism for green finance should be established.

This includes expanding dedicated relending or rediscounting facilities for transition finance and setting up fiscal-backed green finance risk-sharing or compensation mechanisms to encourage financial institutions to expand green and transition financing. At the same time, green finance performance should be more systematically incorporated into the macroprudential assessment framework, while regulatory oversight of greenwashing practices should be strengthened to ensure a balanced and durable system combining both incentives and constraints.

6. Improve investors’ green awareness and mainstream green investment opportunities

Most investors possess a limited understanding of green investment logic, climate risk transmission mechanisms, and green asset valuation methods. Green investment has not been systematically integrated into investment decision-making frameworks. The difficulty in quantifying environmental benefits and the extended return cycles of green projects diminish the appeal of green assets in capital markets, leading to weak demand for green financial products and constraining the deep development of the green finance market.

7. Strengthen specialised green finance talent, including through incentive systems

The growth of green finance has created surging demand for professionals skilled in ESG analysis, climate risk assessment, carbon accounting, and green product design. However, the current higher education training system lags, professional certification mechanisms are inadequate, and existing personnel lack sufficient green finance knowledge reserves. Expanding knowledge and awareness in financial institutions can be linked to compensation benefits (e.g., performance targets) and other incentives.

8. Strengthen international cooperation for green finance standards and policy coordination

This could include the advancement of mutual recognition of Green Electricity Certificates (GECs) and potentially green metals certificates to support the development of green trade, with particular emphasis on institutional alignment with the European Union and ASEAN economies. By promoting interoperability between GECs and international renewable energy certificate schemes, export-oriented firms can be better supported in addressing green trade barriers such as carbon border adjustment mechanisms.

At the same time, international cooperation should be deepened to support green finance development in emerging markets, particularly under the Belt and Road Initiative. Building on existing achievements such as the Multilateral Common Ground Taxonomy (M-CGT), China should continue to promote compatibility and mutual recognition between its domestic green finance standards and mainstream international frameworks

Figure 12: Recommended actions for China’s green finance development

About the authors

Fang Yang is an Associate Professor at Xiamen University in China and a visiting professor at the Griffith Asia Institute of Griffith University in Australia. She holds a PhD in energy economics from Xiamen University. Fang’s research focuses on energy economics, climate change economics, and the Green Belt and Road Initiative (BRI), with years of experience in energy industry management and extensive practical experience in government departments, as well as project research expertise. She has published 3 academic monographs and over 20 papers, and presided over more than 10 scientific research projects, including those funded by the National Social Science Foundation and the National Natural Science Foundation of China. In addition to her academic research, she has served as a consulting expert for the Energy Research Institute of the National Development and Reform Commission, China International Engineering Consulting Corporation, State Development & Investment Corporation Smart City Research Institute, and Global Data Asset Council in China.

Jinze Li, CPA, is a Research Assistant at the Griffith Asia Institute, Griffith University (Brisbane, Australia). He holds a PhD in Finance from Griffith University and contributes strong expertise in quantitative methods and data analysis to multidisciplinary research projects.

His research spans finance and accounting, with particular interests in asset pricing, investor sentiment, emerging markets, and corporate finance. Jinze has published in leading peer-reviewed journals, including Applied Economics and the Journal of International Financial Markets, Institutions and Money. His current work focuses on the development of green finance, including policy frameworks, market mechanisms, and data-driven approaches to support sustainable economic transitions in emerging and developing economies.

Professor Christoph Nedopil is Director of the Griffith Asia Institute and Professor of Economics at Griffith University. He is also Visiting Faculty at Singapore Management University and the Fanhai International School of Finance (Fudan University).He is also acting director of the Green Finance & Development Center founded at FISF Fudan University. His research focuses on green and sustainable finance and development economics, and he regularly advises governments, financial institutions, enterprises, and civil society on advancing sustainable finance practices.

Christoph is lead author of the UNDP SDG Finance Taxonomy, the G20 Innovative Climate Finance Solutions report, and the Green Development Guidance of the BRI Green Development Coalition under China’s Ministry of Ecology and Environment. He has authored four books and published in Science and other leading journals. He is frequently quoted by Financial Times, The Economist, Bloomberg, and Reuters. Previously, he worked with the World Bank and Germany’s GIZ.

About Griffith Asia Institute

Griffith Asia Institute (GAI) at Griffith University, Brisbane, Australia, is an internationally recognised institute providing knowledge and solutions for sustainable development in the Asia-Pacific. With a history of over 20 years, GAI has forged strong partnerships with key decision-makers in business, policy and with research institutions across the region. With over 80 faculty members and 50 adjunct members, GAI works in multidisciplinary teams and draws on a wide range of technical expertise in energy, finance, policy, and economics, as well as in regional studies, including a strong China component.

GAI is led by Professor Christoph Nedopil Wang and is organised through knowledge and regional hubs:

The Green Transition and Sustainable Development Hub addresses major challenges and opportunities for Asian and Pacific economies in addressing SDGs related to climate, life on land, life in the sea, partnerships, infrastructure and energy.

The Governance and Diplomacy Hub addresses major challenges and opportunities in the region for peaceful co-existence, diplomacy, inclusive governance, policymaking and institution building.

The Inclusive Growth and Rural Development Hub addresses major challenges and opportunities in the region regarding currently underserved communities (e.g., women, indigenous, youth, rural, or people with disabilities).

The four regional hubs address major regional and country-specific challenges and opportunities in (1) Southeast Asia, (2) South Asia, (3) Pacific and (4) China and the Region, each with its own hub lead.

https://www.griffith.edu.au/asia-institute

About the Green Finance & Development Center

The Green Finance & Development Center (GFDC) is a leading research center that provides advisory, research and capacity building for financial institutions and regulators for green and sustainable finance in China and internationally.

The GFDC works at the intersection of finance, policy, and industry to accelerate the development and use of green and sustainable finance instruments to address the climate and biodiversity crisis, as well as contribute to better social development opportunities.

The topics of our work at the Green Finance & Development Center respond to the needs and developments of the financial markets and related policies in China and internationally, while we also aim to provide evidence-based advisory and research for future policies and strategies to accelerate the greening of finance in policy and practice.

The Green Finance & Development Center was founded in 2021 by Christoph Nedopil Wang. It is associated with the Fanhai International School of Finance (FISF) at Fudan University in Shanghai, PR China.

[1] Nedopil, C. & Song, Z. “China Green Finance Status and Trends 2022-23”. January 2023. https://cciced.eco/wp-content/uploads/2023/01/GFDC-2023_China-Green-Finance-Trends-and-Opportunities.pdf

[2] Zhang, J., Song, Z. & Nedopil, C. “China Green Finance Status and Trends 2023-2024”. March 2024. DOI: 10.25904/1912/5205

[3] Yue, M. & Nedopil, C. “China green finance status and trends 2024-2025”. March 2025. https://research-repository.griffith.edu.au/items/8f54a3e6-274f-462e-8d19-a6caa2e037e8

[4] Ministry of Foreign Affairs of the People’s Republic of China. “Communique of the Fourth Plenary Session of the 20th Central Committee of the Communist Party of China.” October 2025. https://www.fmprc.gov.cn/eng/xw/zyxw/202510/t20251023_11739505.html