China Belt and Road Initiative (BRI) Investment Report 2025

Key findings

- 2025 saw the highest BRI engagement ever for any year, with USD 128.4 billion in construction contracts and about USD 85.2 billion in investments;

- China’s energy-related engagement in 2025 was the highest in any period since the BRI’s inception, reaching USD93.9 billion, more than double than in 2024;

- China’s 2025 BRI energy engagement was the dirtiest and greenest:

o Oil and gas engagement surged to about USD71.5 billion, more than triple the previous record year 2024;

o Green energy engagement reached new records with USD 18.3 billion in wind, solar, and waste-to-energy projects and planned capacity of over 22 GW of green energy; - China continued to invest in coal-related activities through the construction of coal mine infrastructure;

- The metals and mining sector reached new records, surpassing 2024 (which itself was a record year) with about USD 32.6 billion – mostly through investments and in minerals processing (about USD 15 billion into mining) with a focus on Kazakhstan;

- Copper, in support of data centres, saw a significant surge of Chinese investment in the second half of 2025;

- The technology and manufacturing sector also broke records and reached almost USD 28.7 billion with high-tech engagements in data centres, EV batteries and in hydrogen (in Nigeria);

- Africa topped the rank of BRI engagement, reaching USD 61.2 billion, a plus of 283 per cent; countries with the highest construction engagement were Nigeria (USD 24.6 billion), the Republic of Congo (USD 23.1 billion), Saudi Arabia (USD 19.8 billion), and Iraq (USD 4.5 billion).

- Part of Chinese Africa engagement may be explained by lower US tariffs in Africa compared to Asia;

- BRI investments in 2025 were driven by private sector companies, dominated by East Hope Group, Xinfa Group and Longi Green Energy; construction was dominated by SOEs

- Since its establishment in 2013, cumulative BRI engagement reached USD 1.399 trillion, with about USD 837 billion in construction contracts, and USD 561 billion in non-financial investments;

- For 2026, I see continued expansion of Chinese BRI engagement with a focus on energy, mining, and new technologies;

- Global trade and investment volatility will potentially spur further investment for supply chain resilience and alternative export markets for Chinese companies

China’s finance and investments in the Belt and Road Initiative (BRI)

Preliminary data on Chinese engagement in the 150 countries of the Belt and Road Initiative[1] through investments and construction contracts show record levels:

- USD 128.4 billion (+81 per cent compared to 2024) in construction contracts

- USD 85.2 billion (+62 per cent compared to 2024) in investment[2]

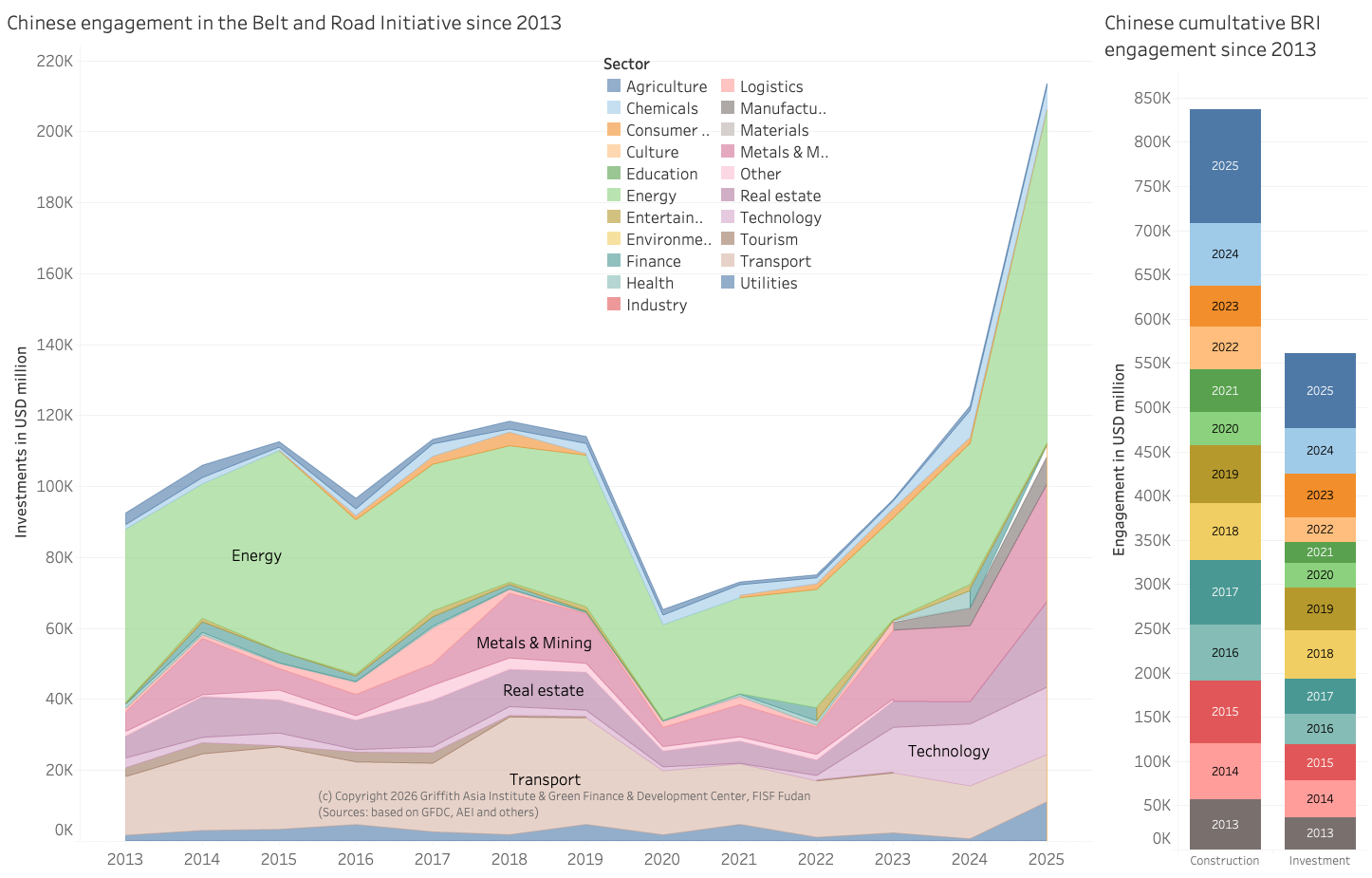

This equals a total engagement of USD 213.5 billion through construction contracts and investments in about 350 deals in 2025 (+19 per cent in deal numbers compared to 2024) (see Figure 1).

Cumulatively, Chinese BRI engagement has reached USD 1.399 trillion since 2013, of which USD 837 billion is in construction and USD 561 billion in investments.

| About the data and methodology: In December 2025, the Ministry of Commerce (MOFCOM) released new BRI engagement statistics covering the period of January to November 2025[3]. According to these data, Chinese enterprises invested about USD 35.7 billion in non-financial direct investments in Belt and Road partner countries – an increase of 18.4 per cent. At the same time, the value of newly-signed project contracts by Chinese enterprises in Belt and Road partner countries was USD 201.7 billion (an increase of 20.4 per cent). While the MOFCOM data are relevant and confirm the trends, the granularity and definitions of BRI engagements are not transparent, including what counts as BRI countries. For this report, BRI engagements are defined as those Chinese construction and investment deals in countries that we have identified as having an active Memorandum of Understanding (MoU) with China to cooperate under the BRI at the time of the report. To stay consistent with data over time and avoid an inflation/deflation of the value of BRI engagement across time simply by adding/subtracting countries that enter or exit the BRI in each given year, the analysis counts Chinese engagement in all current BRI members across the whole time, no matter when they signed the MoU (thus, if the Syrian Republic signed a BRI MoU in 2022, the analysis counts all Chinese engagement since the initiation of the BRI in 2013 as BRI engagement in Syria). A similar approach is used for countries that exited the BRI (i.e., if Italy exited the BRI in 2023, the analysis does not count any Chinese engagement in Italy to the BRI engagement for any year). The definition of BRI countries currently includes 150 countries that have signed a cooperation agreement with China to work under the framework of the Belt and Road Initiative (BRI) by December 2025. Our data since 2024 has been collected based on a rigorous independent collection process: we include projects with validated credible sources or two independent sources. We include projects with a signed contract for implementation or clear announcements of investments (e.g., stock market announcements). We consistently aim to include projects worth about USD20 million. The data until 2023 was reliant on the China Global Investment Tracker (CGIT), published by the American Enterprise Institute[4], which only includes deals larger than USD 100 million. We have significantly expanded the original CGIT data based on our research, also for the years until 2023. As with most data, they tend to be imperfect and need regular updating. |

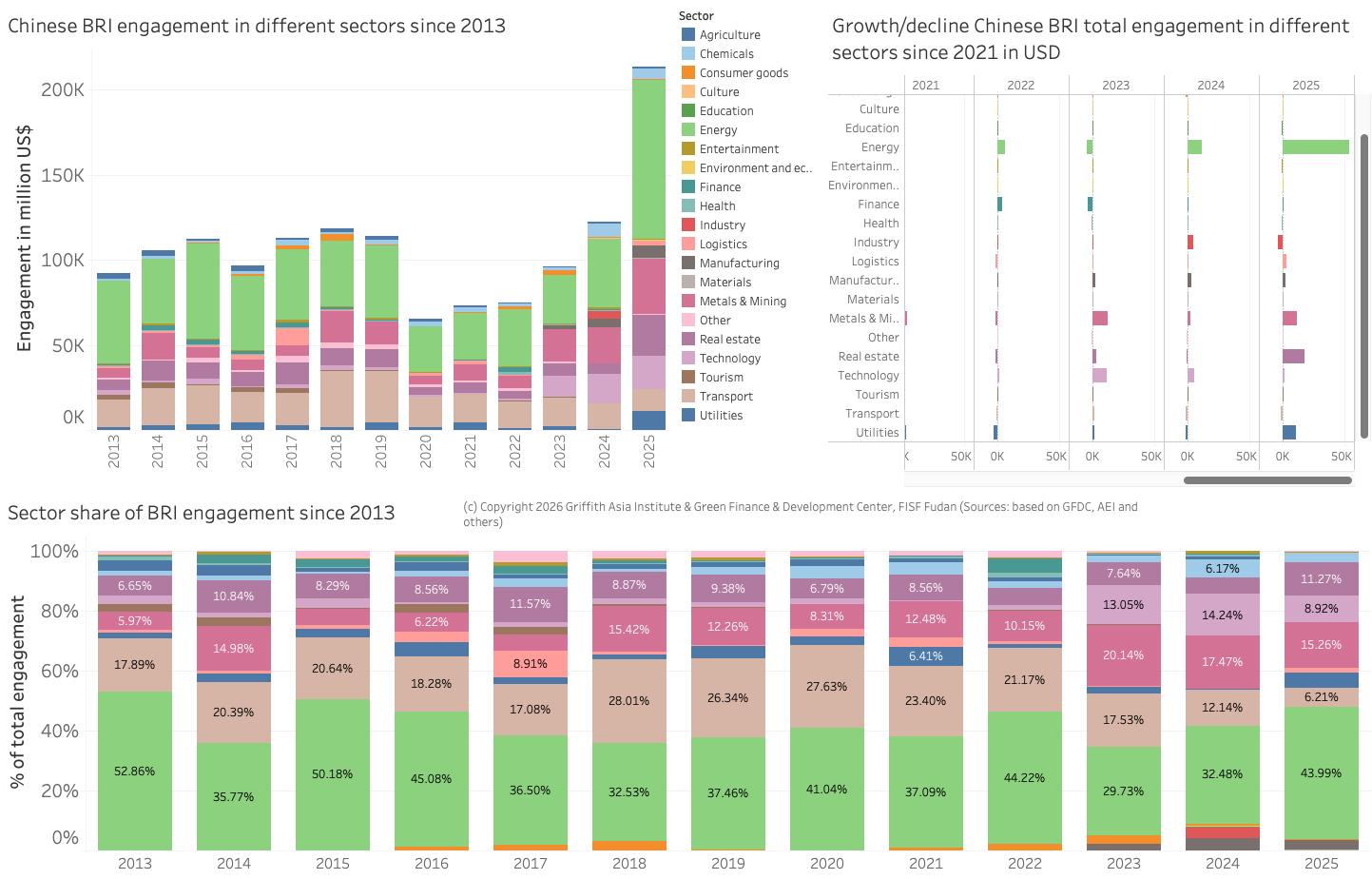

Figure 1: China’s BRI engagement by sector since 2013 (left) and cumulative (right)

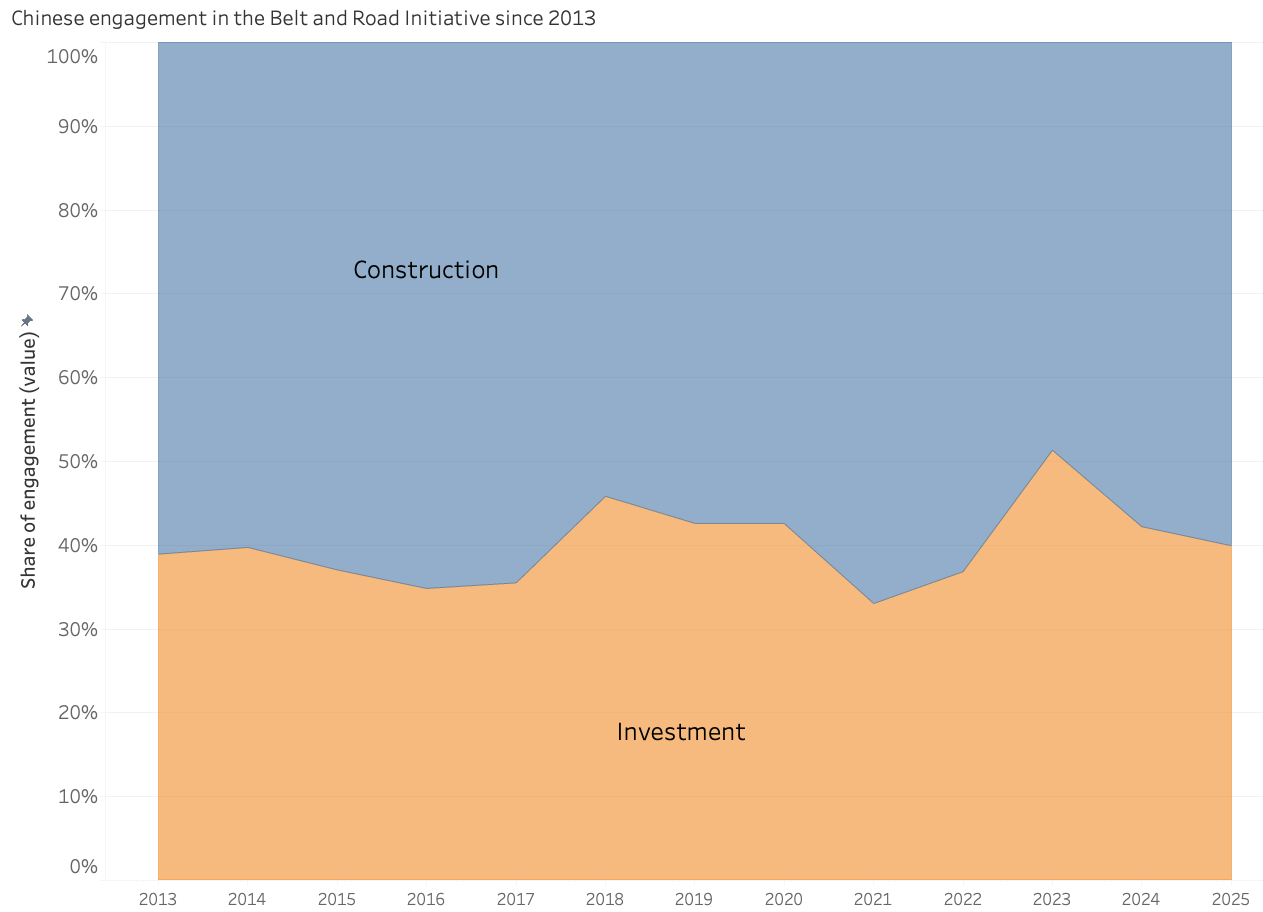

Share of construction in China’s BRI increases, driven by high-value construction contracts

The share of Chinese engagement in the BRI through construction reached about 60 per cent and increased compared to 2024, driven by high construction volume increases. This compares to about a share of 40 per cent for investment in Chinese BRI engagement.

Construction contracts that are often financed through loans provided by Chinese financial institutions and/or contractors with the project, sometimes receiving guarantees through the host country’s government institutions, potentially backed up by resources (e.g., oil, gas) (see Figure 2).

Figure 2: Share of construction and investment engagement in the BRI 2013-2024

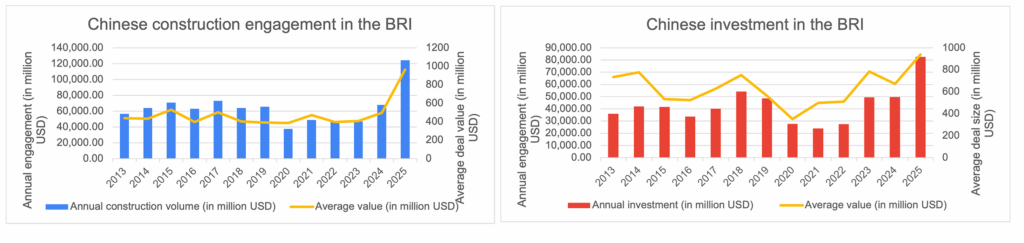

Deal sizes are at record high levels for both investments and construction

The average deal size for investments with a value larger than USD 100 million grew to record levels of USD 939 million in 2025 (from USD 672 million in 2024)[5]. The value is about three times higher than in 2020 (during the first year of COVID).

For construction projects, the average deal size in 2025 increased to USD 964 million, up from USD 496 million in 2024 (see Figure 3).

Both developments are driven by single large projects, such as a USD 20 billion construction project in Nigeria and two investment projects valued at more than USD 5 billion, both in Kazakhstan.

With this, the “small yet beautiful projects”(小而美in the BRI propagated through official channels during COVID should be seen as bygone.

It is important to note (as seen later in the report) that many large infrastructure projects are resource-backed deals (e.g., oil, gas) and thus revenue-generating, as compared to fiscal spending in host countries (e.g., road construction). This provides relatively lower financial risks for Chinese counterparts in supporting and potentially financing these construction contracts.

Figure 3: Deal size of Chinese engagement in the BRI of deals larger than USD100 million since 2013

Regional and country analysis of Chinese BRI engagement

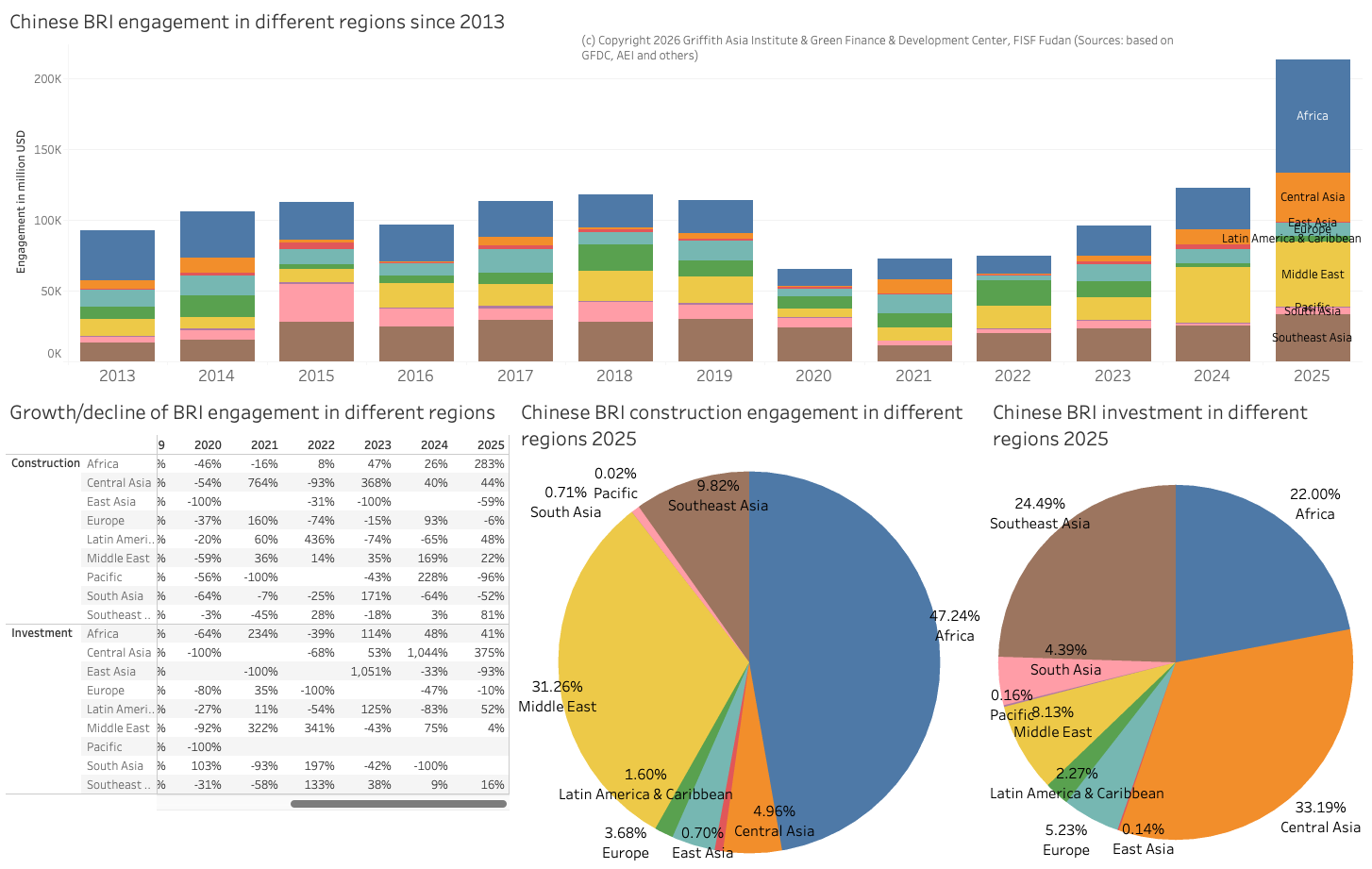

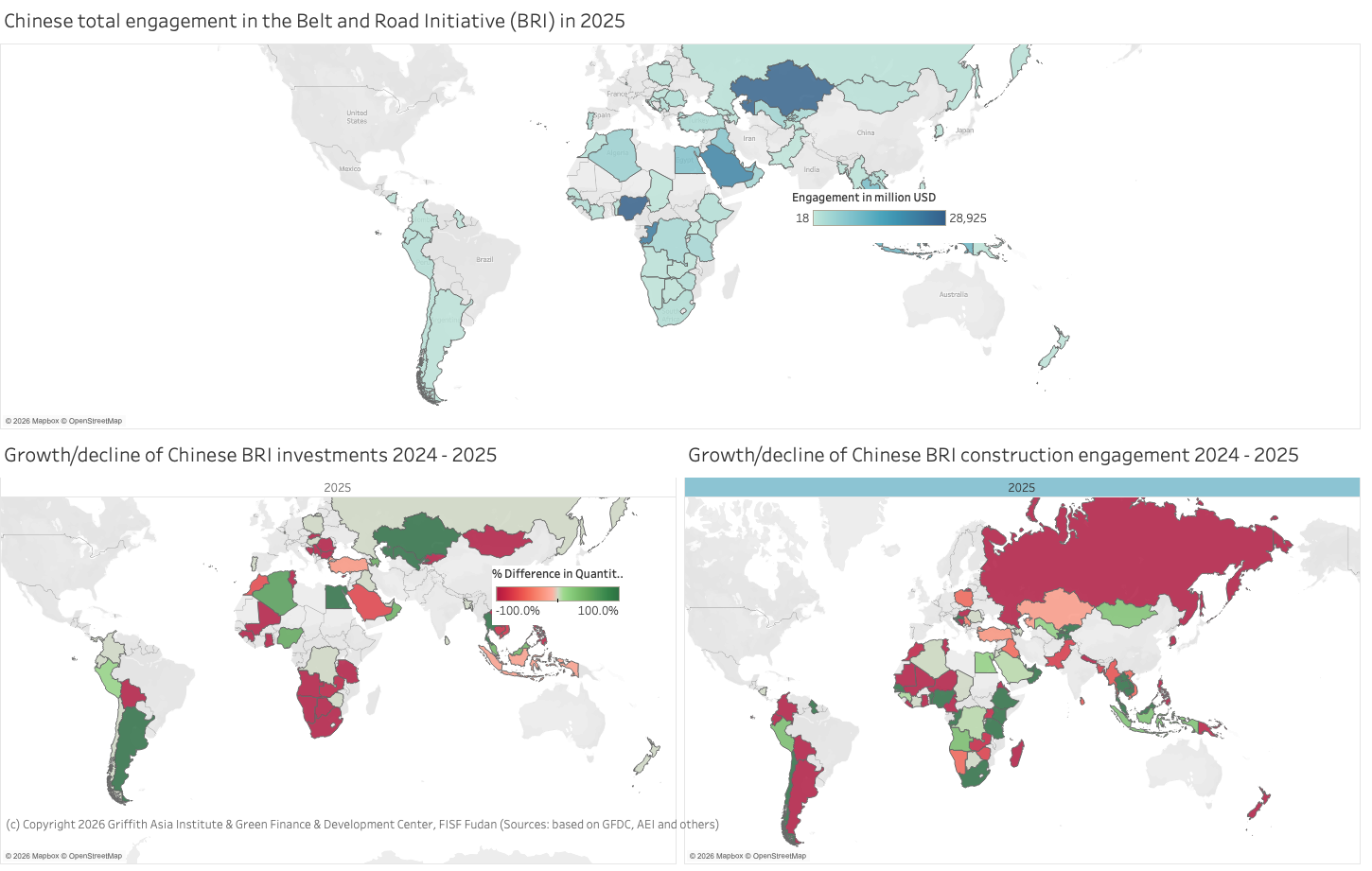

Africa almost triples Chinese BRI engagement in 2025, Central Asia investment almost quadruples, and Pacific engagement vanishes

Chinese BRI engagement was not evenly distributed among all regions[6]. China’s construction engagement across multiple regions increased significantly compared to 2024.

- Africa: plus 283 per cent to USD 61.2 billion

- Southeast Asia: plus 81 per cent to USD 12.7 billion

- Latin America: plus 48 per cent to USD 2.1 billion

This compares to significant drops in the Pacific (minus 96 per cent) and East Asia (minus 59 per cent).

In Chinese BRI investment across the region, East Asia similarly dropped almost off the radar (minus 93 per cent). This compares to an increase of 375 per cent of Chinese investment in Central Asia (this is on top of a 1,044 per cent (!) increase in 2024, mostly driven by metals and mining-related investment, reaching a value of USD 28.3 billion.

The region with the absolute largest construction engagement was also Africa, with the Middle East coming in second with USD 39.4 billion in engagement.

A reason for Africa’s strong engagement may be US tariffs, which are lower in some parts of Africa compared to e.g., Vietnam. An example is the decision by Boway Alloys to scrap a plant in Vietnam to invest in Morocco instead – explicitly to take advantage of the 10% US tariff in Morrocco.[7]

For investment, Central Asia was also the largest recipient of Chinese money, followed by Southeast Asia (USD 20.9 billion) and Africa (USD 18.8 billion) (see Figure 4).

Pacific countries continue to see low Chinese engagement, remaining at the lowest values in the past 10 years for investment and construction. Latin American countries, despite increases, continue to see little Chinese engagement (USD 2.1 billion in construction and USD 1.9 billion in investment). However, China is strongly engaged in Latin America with over USD 53 billion investment in Brazil in 2025, albeit Brazil is not a BRI country.

Figure 4: Chinese engagement in different BRI regions since 2013 (top), year-on-year change (bottom left), and regional share for construction and investment in H1 2025

China’s financing and investment spread across 89 BRI countries in 2025 (up from 87 in 2024), with 57 countries receiving investments and 66 with construction engagement.

The country with the highest construction volume in 2025 was Nigeria with about USD 24.6 billion (up from 1.8 billion in 2024), followed by the Republic of Congo (USD 23.1 billion), Saudi Arabia (USD 19.8 billion), and Iraq (USD 4.5 billion). Other key BRI countries, such as Indonesia and Pakistan, gave USD 3.3 billion and USD 39 million in construction contracts, respectively.

Regarding BRI investments, Kazakhstan was the single largest recipient with about USD 25.8 billion in investments in 2025, followed by Egypt (USD 10.2 billion) and Thailand (USD 8.5 billion). Pakistan, a key partner of China in the first phases of the BRI, received no investment.

17 countries saw a 100 per cent drop in BRI engagement compared to 2024, including Cameroon, Tunisia, Nepal, and Niger (the Philippines saw a 96 per cent drop). China’s engagement in Pakistan for the China-Pakistan Economic Corridor (CPEC) dropped by 77 per cent (see Figure 5).

The countries with the largest growth of BRI engagement were Ethiopia (+4,827 per cent), Democratic Republic of Congo (+3,937 per cent), Romania (+3,171 per cent), Ecuador (+3,062 per cent), and Sri Lanka (+1,590 per cent).

Unlike in the years before, Russia received significant investment from China worth USD 674 million.

Figure 5: Trends of Chinese BRI engagement across different countries 2025 (top) and comparison of 2024 H1 and 2025 H1 investments (bottom left) and construction engagement (bottom right)

Sector trends of BRI engagement

In 2025, particularly the energy sector (+ USD 54.1 billion), real estate (+USD 17.8 billion), metals & mining (+11.2 billion) and utilities (+USD 10,4 billion) grew compared to 2024.

The focus of China’s overseas BRI engagement continued to be in energy (43 per cent of total, a growth from 32.5 per cent in 2024). Compared to the early years of the BRI, the transport sector dropped to its lowest level of only 6.2 per cent share of BRI engagement (compared to e.g., 12 per cent in 2024 and a high of 28 per cent in 2018).

Meanwhile, the metals and mining sector kept its role as the second largest sector with about 15.3 per cent of total, while the share of the technology sector contracted slightly to 9 per cent (despite an absolute growth), giving way to the real estate sector reaching 11.3 per cent of total engagement (see Figure 6).

Figure 6: BRI investments in different sectors since 2013

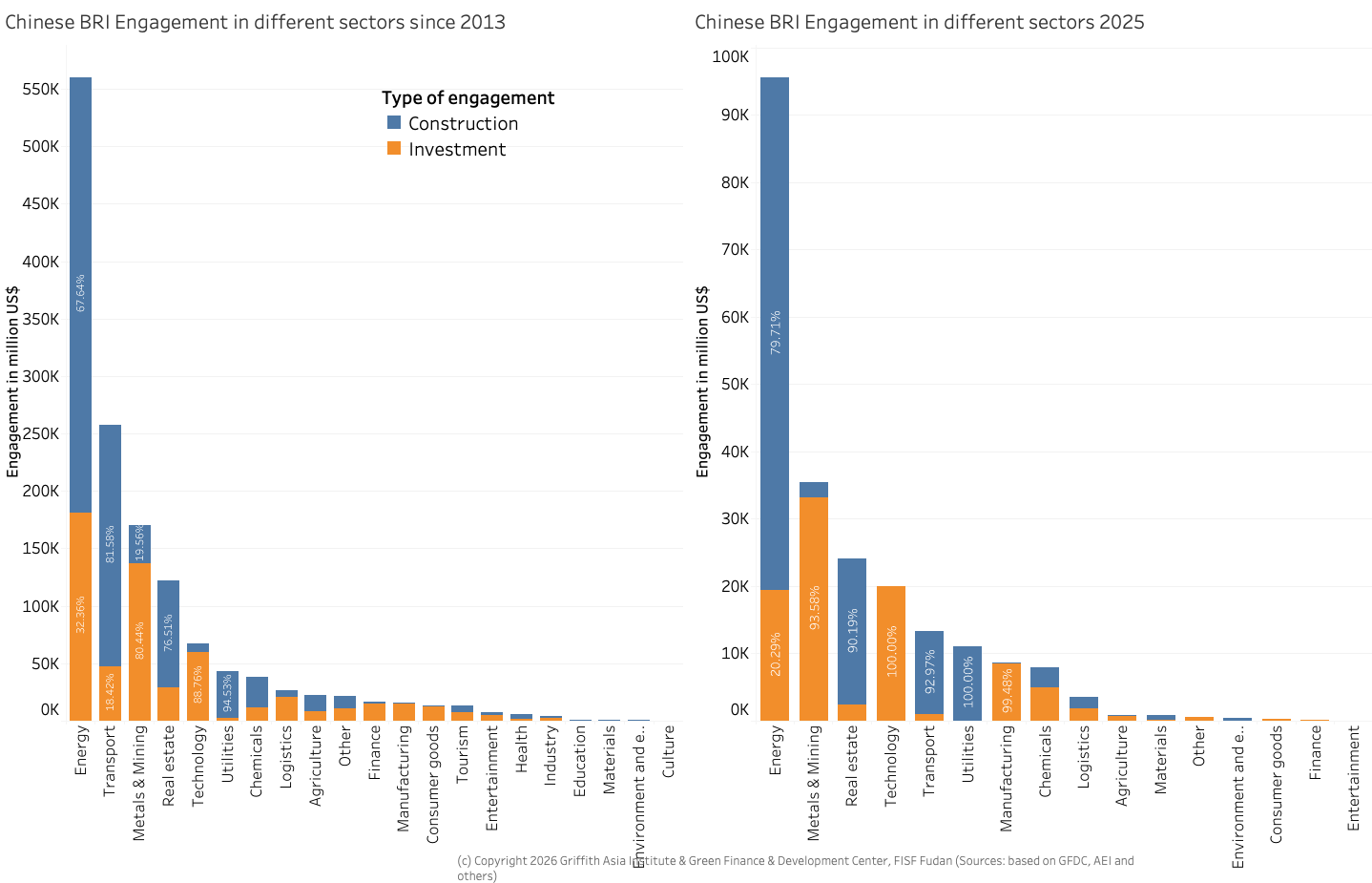

When comparing construction and investment in different sectors, it becomes clear that in mining and technology, Chinese firms are prioritising equity investments (94 per cent in 2025); meanwhile, energy investments continue to be dominated by construction deals (80 per cent) rather than equity-based investments. Similarly, real estate deals and utilities are predominantly construction deals (see Figure 7).

Figure 7: Chinese BRI engagement in different sectors through construction and investment since 2013 (left) and in 2025 (right)

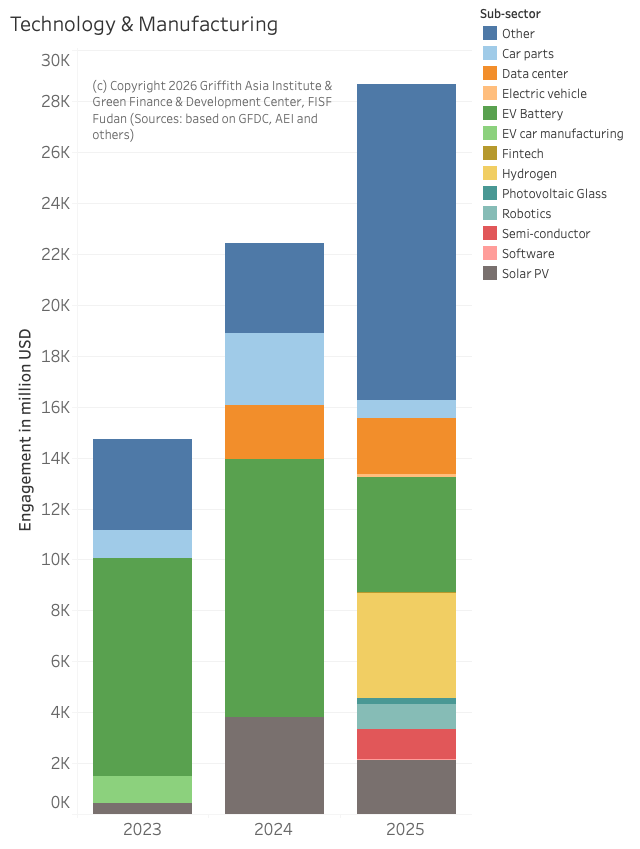

Technology and manufacturing

Technology and manufacturing remain key growth sectors, with Chinese engagement in BRI countries growing by about 27 per cent compared to 2024 to USD 28.7 billion. Apart from general manufacturing, the technology investment saw strong increases is semi-conductor engagement, while solar PV manufacturing engagement dropped compared to 2024. A significant engagement by Longi in green hydrogen development was seen in Nigeria[8] (see Figure 8).

Other notable engagements include a USD 2.1 billion investment by China Aviation Lithium Battery (CALB) in a lithium battery factory in Portugal, or a USD 700 million solar PV glass production base in Egypt by Xinyi Glass Holding. As mentioned above, TikTok invested more than USD 37 billion in a data centre in Brazil (outside of the BRI).

Figure 8: Technology and manufacturing-related BRI engagement since 2023

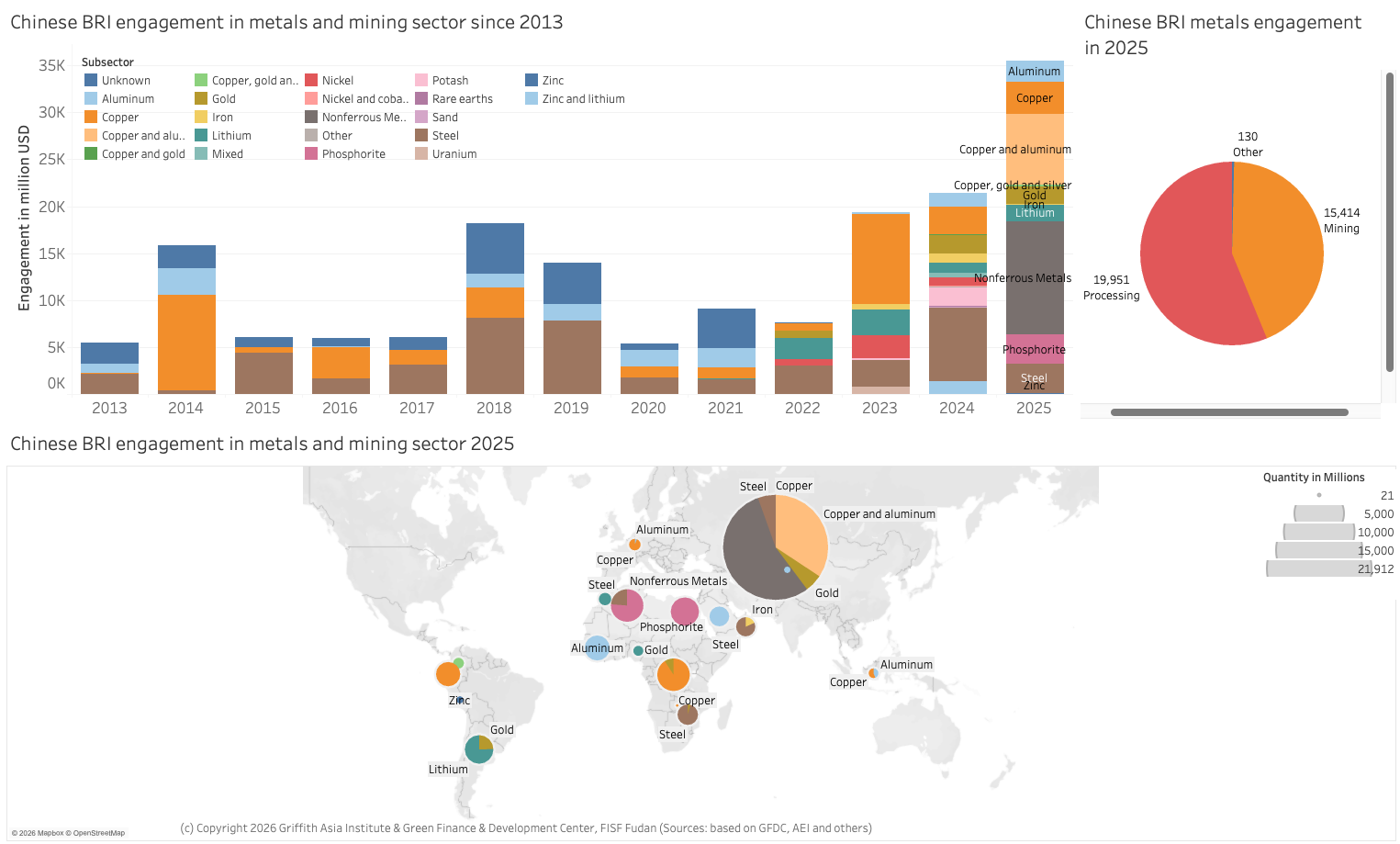

Metals and mining

Another important growth sector of strategic importance to China is metals and mining, where China’s engagement reached a record high of USD 32.6 billion in 2025. Kazakhstan saw the most important engagement through USD 12 billion in aluminium and another 7.5 billion in copper. Compared to previous years, little Chinese engagement was seen in Indonesia, except for an aluminium-related and a copper-related investment.

An interesting development is the focus on copper in the second half of 2025. An explanation can be the relation of copper to data centres for AI to support power networks, circuit boards, or cooling systems.

It is important to note that in 2025, the share of mining compared to processing facilities (e.g., smelters) was about 61 per cent, with 39 per cent of the investment (about USD 15 billion) going to exploitation/mining-related activities (see Figure 9).

Figure 9: Chinese BRI engagement in metals and mining since 2013

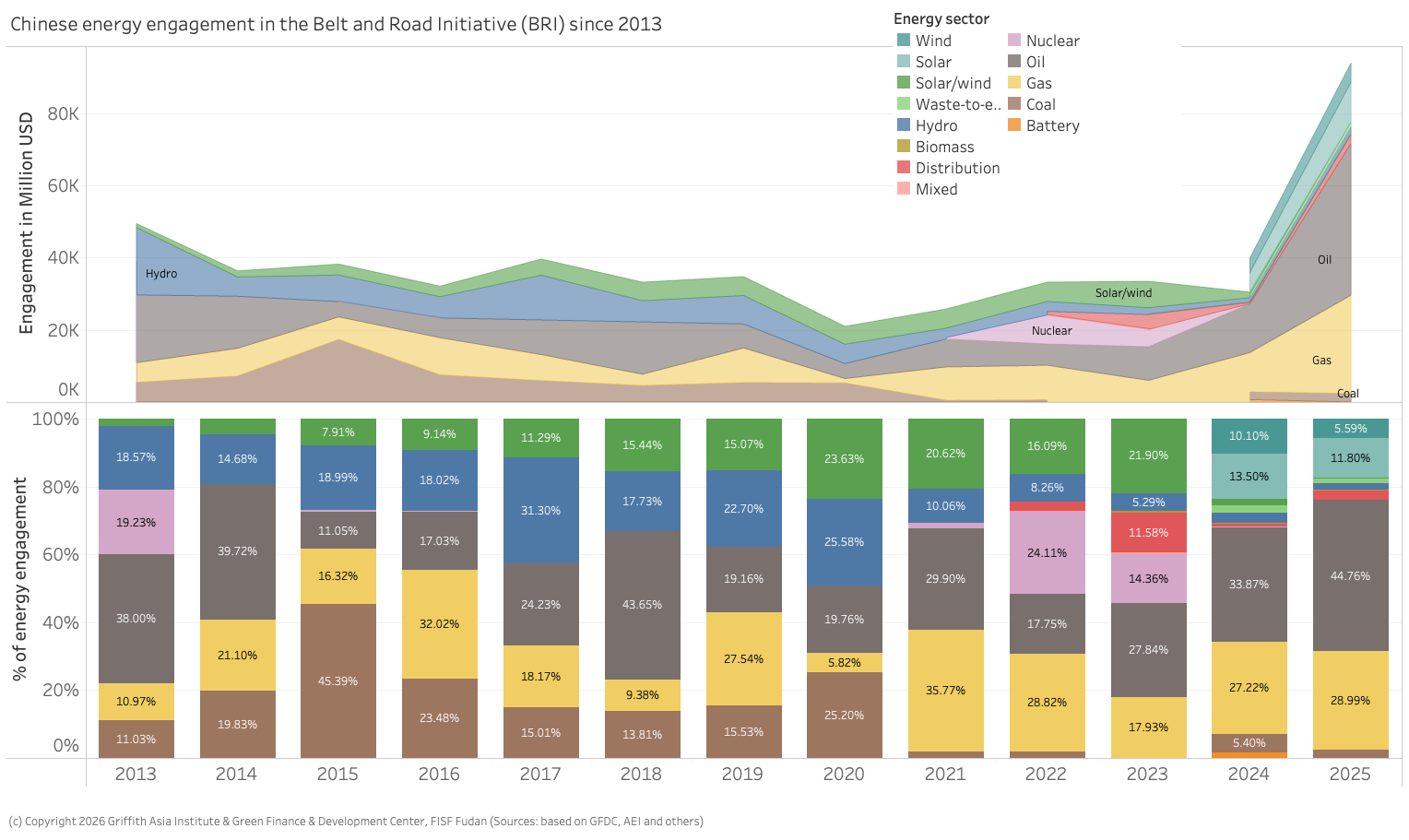

Energy-related engagement in the BRI at the highest levels ever recorded, with an increase in absolute green, but a faster increase in gas-related engagement

In 2025, China’s energy engagement was about USD93.9 billion, more than twice than in the previous full record year 2024.

China’s engagement in green energy has also seen the highest since 2013 – with USD 18.3 billion in wind, solar, and waste-to-energy plus USD 3.1 billion in hydro.

At the same time, China significantly expanded its engagement in fossil fuels, particularly gas, but also coal (through coal mining) to over USD 71.5 billion – almost triple the previous record year 2024.

Engagement in distribution systems (e.g., substations, power lines, storage) was about USD 2.5 billion (see Figure 10).

Cumulatively, since 2013, oil engagement topped gas engagement with USD 156 billion versus USD 113 billion. Solar and wind engagement with USD 72.9 billion has surpassed coal with about USD 64 billion (hydro adds another USD 69 billion).

The next paragraphs further analyse China’s energy engagement.

Figure 10: Chinese total energy engagement in the Belt and Road Initiative (BRI) since 2013

Coal

Following China’s announcement in September 2021 to not to build new coal-fired power plants, China continued to engage in new coal-fired power projects that seem to progress (e.g., Indonesia, Bangladesh Barisal 2, Gacko II in Bosnia).

2025 saw a continued engagement in coal-related engagement through mining operations. PowerChina was engaged in several projects in Mongolia and China Railway in Indonesia (all through construction contracts). Altogether, over USD 2.3 billion in contracts for coal-related activities were identified.

Oil and gas

Oil and gas engagement rose significantly to over USD 42 billion and USD 27 billion, respectively, in 2025 (up from USD 24.3 billion for both in all of 2024). In 2025, fossil fuel engagement constituted over 74 per cent of Chinese overseas energy engagement. This is the highest share of fossil fuel engagement since 2014.

As for investments, a major deal was the USD 3.7 billion investment by Sinopec in Sri Lanka to build an oil refinery.

Meanwhile, most gas-related projects were related to construction projects – no gas-related investments were identified. This includes projects, such as the USD 20 billion Ogidibgon Gas Revolution Park in Nigeria and the USD 1.6 billion engagement by Harbin Electric in Saudi Arabia for a gas-fired power plant.

Green energy/hydropower

China’s total engagement in green energy (solar, wind, waste-to-energy) and hydropower reached approximately USD 21.4 billion in 2025, up from USD 12.3 billion in 2024.

Looking at investment only, Chinese green energy and hydropower investment increased to USD 5.9 billion in 2025, upfrom USD 1.5 billion in 2024.

Meanwhile, construction projects related to green energy (including hydropower) increased to USD 13.7 billion in 2025 from USD 10.3 billion in 2024 (see Figure 11).

Figure 11: Chinese energy engagement through investment and construction in the BRI since 2013 by subsector

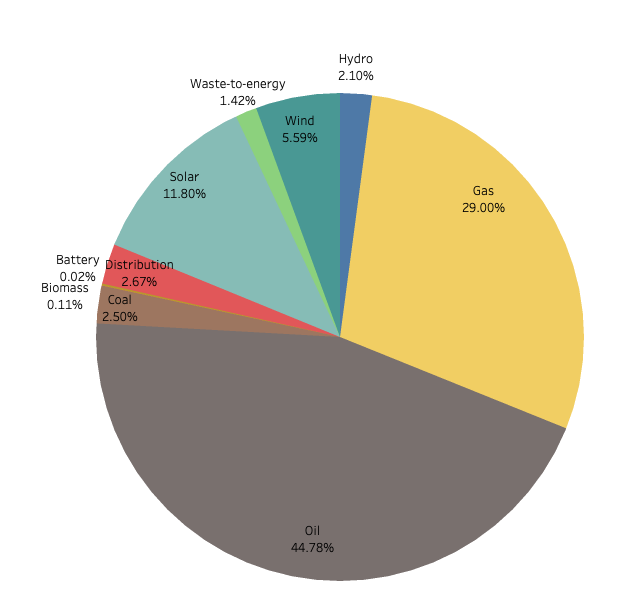

Green energy sources varied

In 2025, a more detailed analysis of green energy sources revealed that China is engaging in a diverse range of energy projects. While solar and wind play an absolutely growing role, in 2025 the majority was fossil fuel related engagement with 29 per cent gas, 45 per cent oil, and 2.5 per cent coal related engagement (see Figure 12).

Figure 12: Chinese renewable energy engagement in the BRI in 2024 by source

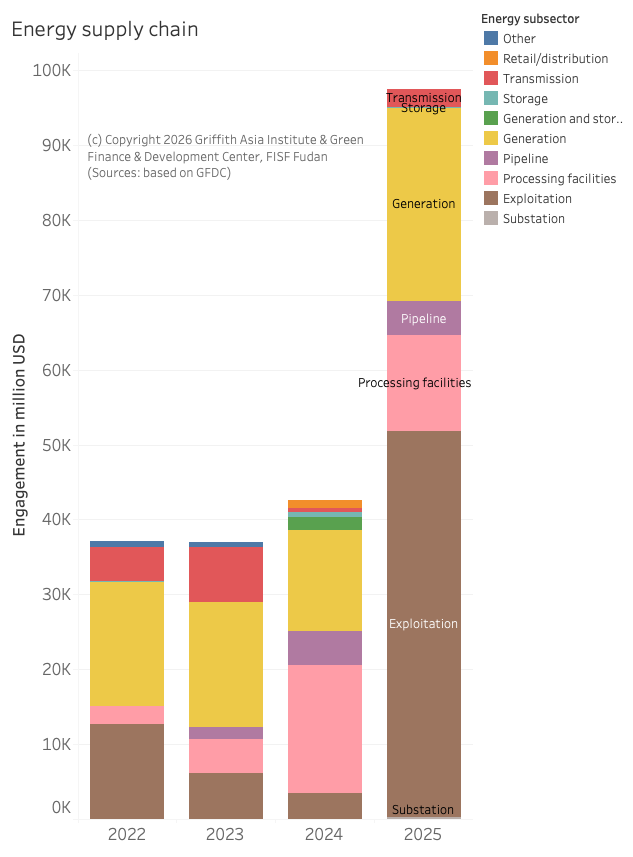

Energy engagement across the supply chain

Since 2022, China’s engagement across the energy supply chain has evolved significantly. While energy generation remained the primary focus in both 2022 and 2023, since 2024 (including in 2025), fossil fuel-related engagement in exploitation (USD 51.4 billion), processing facilities (USD 12.8 billion), and pipeline projects (USD 4.6 billion) were dominant. (see Figure 13).

Figure 13: Energy engagement across the supply chain

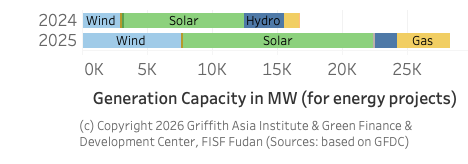

Looking at generation capacity only, Chinese engagement in 2025 almost doubled from 2024 in value (USD 25.8 billion). This allowed an addition of at least 28.2 GW of generation capacity: 14.6 GW in solar, 7.6 GW in wind, 1.6 GW in hydro, and 4 GW in gas projects (see Figure 14).

Figure 14: Energy generation additions in the BRI since 2024

Energy engagement in different countries

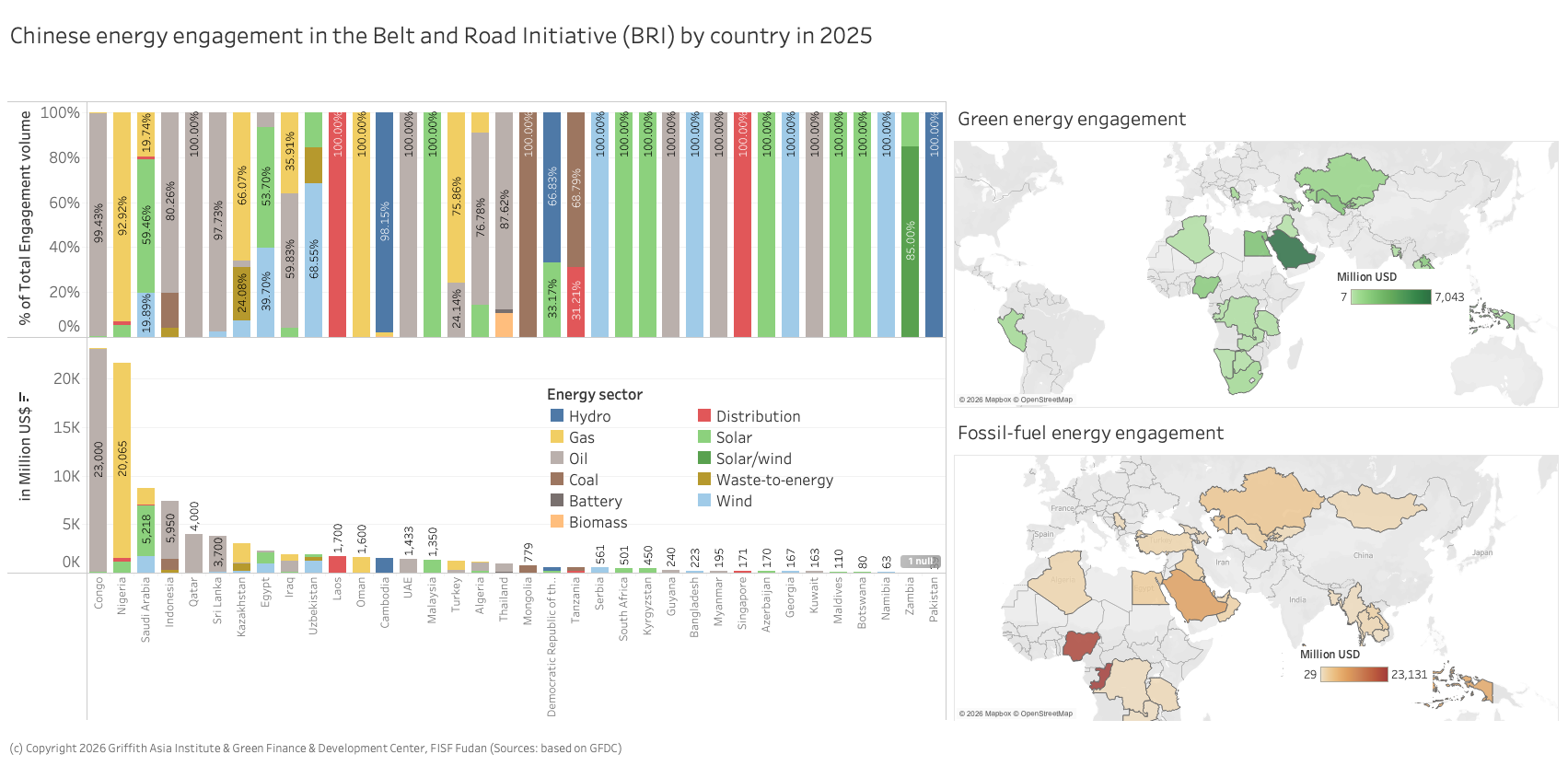

An analysis of China’s energy engagement across BRI countries in 2025 reveals that Congo is the country with the highest Chinese energy engagement, driven by a USD 23 billion oil and gas development agreement between the Republic of Congo (Brazzaville) and Southern Petrochemical Group Yonghua. The goal is to increase the oil production of three oil and gas blocks (Banga Kayo, Holmoni, and Cayo) to 200.000 barrels per day by 2030[9]. Meanwhile, in Nigeria, construction contracts in the Ogidigbon Gas Revolution Industrial Park by China National Chemical Engineering were worth about USD 20 billion. Saudi Arabia saw the largest Chinese engagement in green energy, worth about USD 5.2 billion (see Figure 14).

Cumulatively since 2013, Pakistan is the country with the highest Chinese energy engagement worth over USD 41.5 billion, followed by Saudi Arabia with about USD 40 billion and Nigeria (USD 28 billion).

Figure 15: Chinese energy engagement in the Belt and Road Initiative (BRI) by country in 2025

Transport engagement in the Belt and Road Initiative

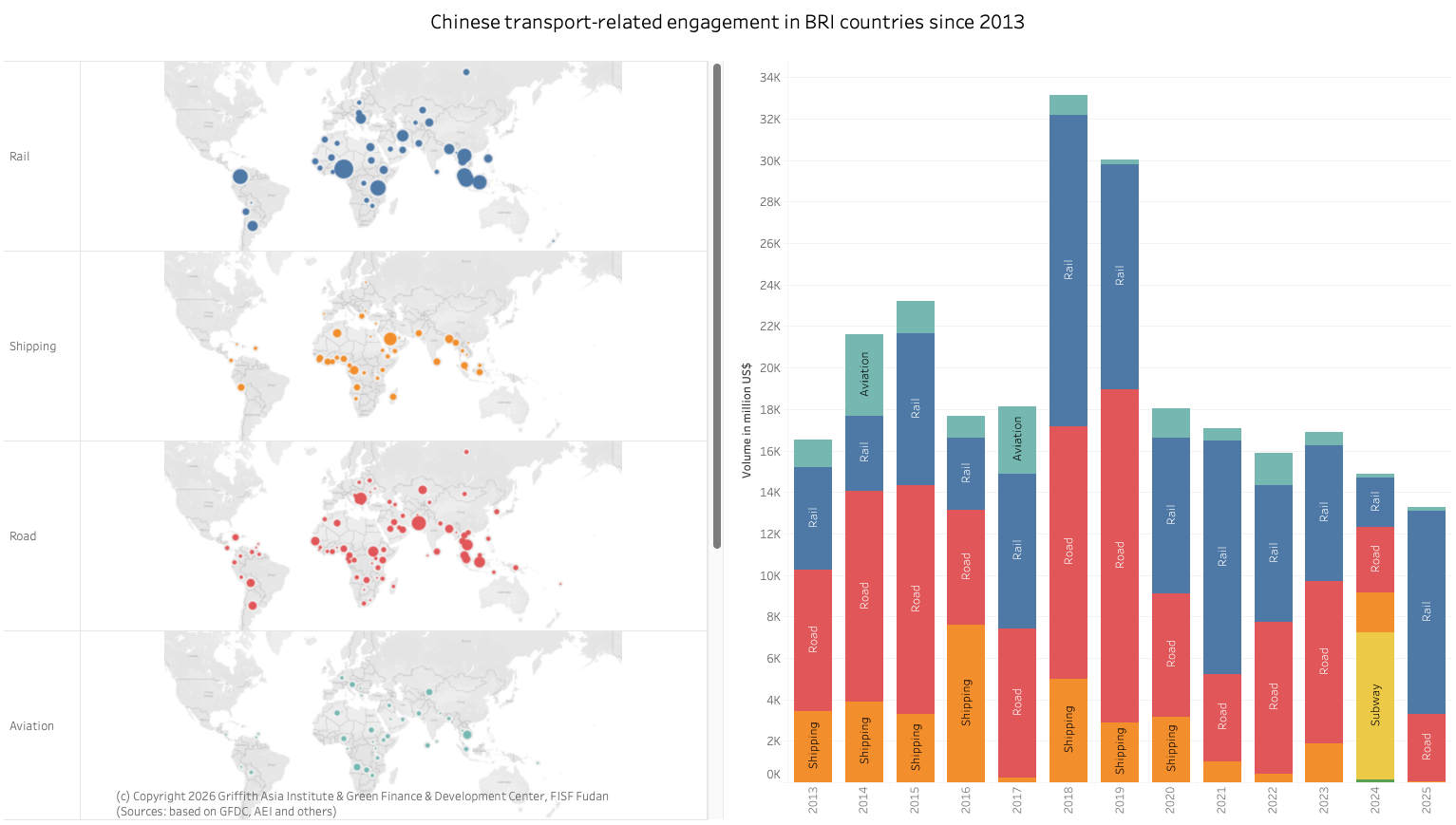

Transport-related engagement has long been a cornerstone of facilitating trade between China and the BRI countries, and trade is a core component of the BRI. To support this, China has invested in and developed projects in road, rail, aviation, shipping, and logistics across the world (see Figure 15).

However, over the past few years, China’s engagement in transport-related projects has steadily decreased, reaching a low of USD 13.3 billion in 2025. Almost all transportation projects (93 per cent) are done through construction contracts (rather than investment).

Aviation: One project was announced, totalling USD 152 million, which is the Punta Verte International Airport in Nicaragua.

Rail: Total rail engagement (including light rail and subway) was worth USD 9.8 billion, where, particularly, the expansion of the Standard Gauge Railway in Tanzania stands out with involvement from China Railway Group Limited (CREC) and China Civil Engineering Construction Corporation (CCECC). In Mexico, China Railway Rolling Stock Corporation (CRRC) won the bid to supply 17 electric units for a light rail in Mexico City.

Road transport: China continues to engage in road construction projects across multiple BRI countries, with a total value of USD 1.7 billion in 2025 H1. However, this marks the lowest volume of road-related engagement in BRI history.

Ports: No shipping project was found in 2025 in BRI countries (outside of the BRI, projects include the acquisition of VAST Infra-crude oil port operator by China Merchants Group valued at USD 448 million in Brazil).

Figure 16: Chinese engagement in BRI transport infrastructure since 2013

Major players in BRI investments

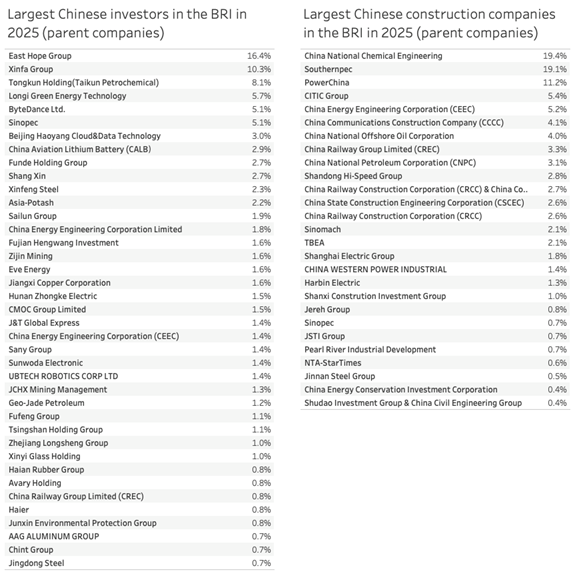

In 2025, Chinese private enterprises reclaimed a dominant role in investment from private enterprises, reversing the trend of the last year (see Table 1).

For investment projects, East Hope Group and Xinfa Group led ahead of Longi Green Energy and Bytedance (all private companies). Sinopec, a state-owned enterprise, ranked sixth.

The Chinese companies most prominently featured in construction projects in the BRI in 2025 was China National Chemical Engineering, followed by the leader in previous years PowerChina.

Construction projects are all dominated by Chinese state-owned enterprises.

Table 1: Major Players in BRI investments in 2025 H1 (parent companies)

China’s BRI investments in a global comparison

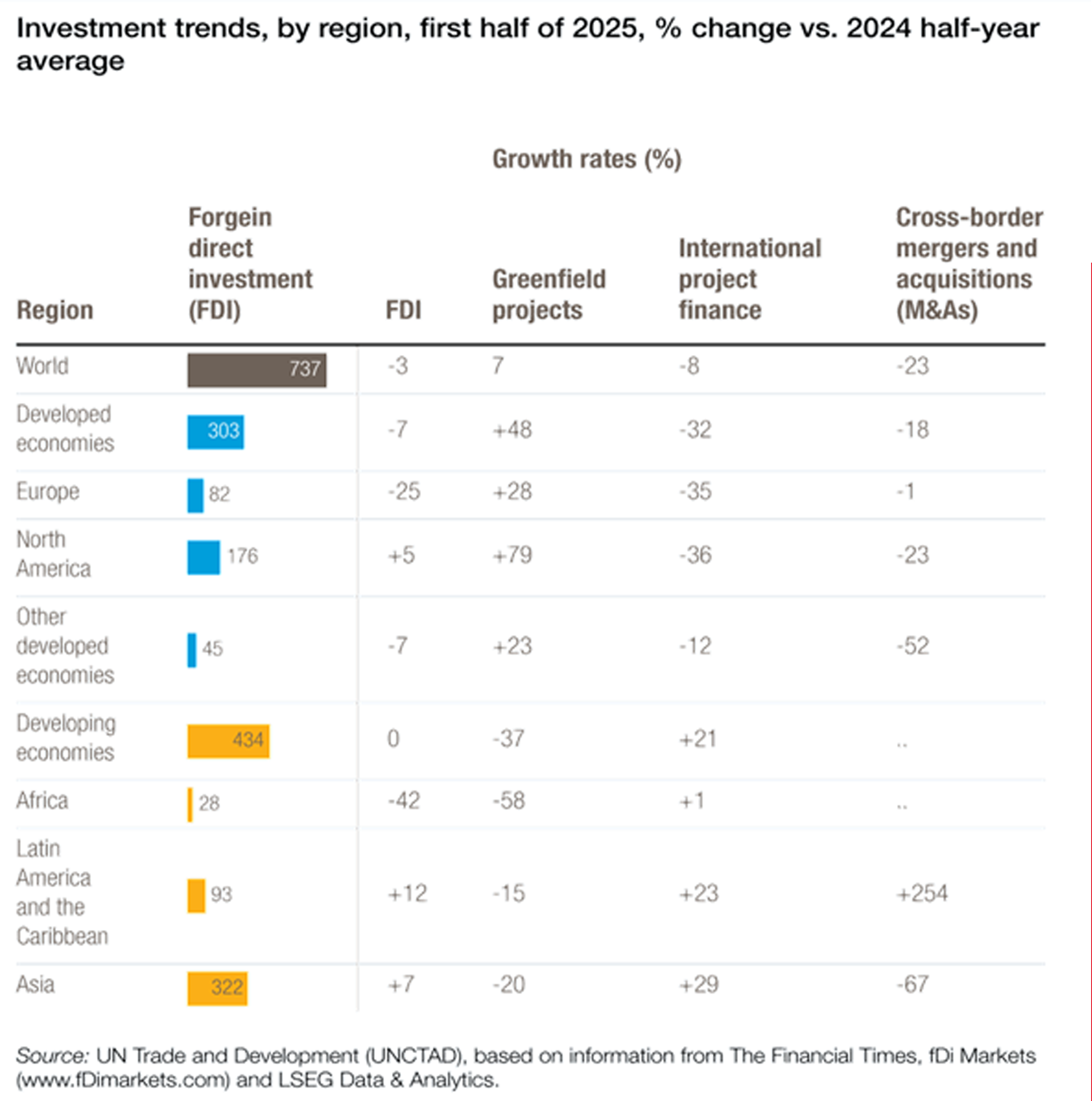

Latest reliable data on FDI in emerging economies encompasses the first half of 2025: FDI markets reports USD 700 billion in worldwide cross-border investment – the third highest capital expenditure figure in a half-year period since 2003.[10] The data show an increase in projects worth over USD 1 billion with a focus on data centres and semiconductor projects (together worth nearly USD 300 billion). Meanwhile, greenfield FDI in renewable energy shrank from USD 147 billion in the first half of 2024 to USD 83 billion in the first half of 2025.

OECD similarly identified USD 663 billion of FDI in the first half of 2025[11], which is a decrease compared to the previous four years (the peak of FDI for the first half of a year was in 2022 and has almost halved since then).

UNCTAD similarly reports a 3 per cent drop of FDI in 2025, driven by a 25 per cent drop in Europe and a 42 per cent drop in Africa[12]. Overall, developing countries received about USD 434 billion in international FDI, similar to the year before (see Figure 17).

While renewable energy investments were the main source of FDI in emerging economies since 2020, their number dropped slightly in the first half of 2025 (see Figure 18).

Figure 17: Regional investment trends in 2025

Figure 18: Number of international projects in developing countries

Outlook for Belt and Road Initiative (BRI) finance and investments

Chinese finance and investments into the Belt and Road Initiative countries in 2025 have accelerated significantly.

For 2026, a further expansion of BRI investments and construction contracts seems possible despite (or because of) global economic headwinds driven by US-led trade impositions. On the one hand, there is a clear need for investments to boost growth to support the green transition both in China and in BRI countries. This provides continued opportunities for mining and minerals processing deals, technology deals (e.g., EV manufacturing, battery manufacturing) and green energy (e.g., energy production and transmission). China refers to these industries (electric vehicles, batteries and renewable energy) as the “New Three”.

Furthermore, global trade volatilities and uncertainties can spur investments in supply chain resilience and exploration of new markets by Chinese companies. However, risks emerge due to the uncertainty of possible activities by global financial institutions with strong US board presence (e.g., World Bank Group, Asian Development Bank), while China-dominated development banks (e.g., AIIB, NDB) should provide infrastructure development opportunities for Chinese contractors.

Nevertheless, I expect Chinese BRI engagement to reach lower levels in 2026 with fewer megadeals.

With strong engagement in sectors requiring significant investment (e.g., mining, manufacturing), and increasing ability to scale energy investment as well as data centres, I expect deal size to also remain large.

Appendix 1: About the BRI

The Belt and Road Initiative (BRI) is China’s main international cooperation and economic strategy. The BRI is also known as the “One Belt One Road” (OBOR), the “Silk Road Economic Belt and the 21st-century Maritime Silk Road” or just the “New Silk Road”. Its Chinese name is 一带一路 (yi dai yi lu). It was announced by Chinese President Xi Jinping in Kazakhstan in October 2013.

The construction of the Belt and Road Initiative is anchored in the Chinese constitution.

Goals of the Belt and Road Initiative—and how to make it green

The BRI has officially “five goals”:

- policy coordination,

- facilities connectivity,

- unimpeded trade,

- financial integration, and

- people-to-people bonds.

Over the past years, the emphasis on developing a “green” and “high-quality” Belt and Road Initiative have accelerated. The Ministry of Environmental Protection (now Ministry of Ecology and Environment) had published the Guidance on Promoting Green Belt and Road already in 2017. The document stresses the relevance of the “ecological civilisation”, “green development concepts”, and “principles of resource efficiency and environmental friendliness” within the five goals of the Belt and Road Initiative.

During the 2019 Belt and Road Forum, green and sustainable development of the Belt and Road Initiative took centre stage, together with debt sustainability. Accordingly, the Ministry of Ecology and Environment jointly initiated the BRI International Green Development Coalition (BRIGC) with international partners. With its 10 working groups, the BRIGC aims to support green development in e.g.,

- green finance

- green transport

- green innovation

- green urbanisation

- green standards

In 2020, the MEE and several relevant ministries backed the Green Development Guidance for BRI Projects Baseline Study published by the Belt and Road Initiative International Green Development Coalition (BRIGC). The Guidance lays out nine recommendations for greening the BRI and an initial project taxonomy (“traffic light system” that distinguishes projects with high environmental risk (red projects) and projects with environmental benefits (“green projects”). In 2021, an Implementation Guide for financial institutions and project developers was published. Also, in 2021, the Green Development Guidelines for Overseas Investment and Cooperation were published by MOFCOM and MEE, while the same ministries published the Guidelines for Ecological Environmental Protection of Foreign Investment Cooperation and Construction Projects in January 2022 to stress relevant environmental risk management practices.

Find an overview of relevant policy documents for the Belt and Road Initiative here.

Appendix 2: Countries of the BRI

According to official information, in December 2024, 149 countries had signed cooperation agreements for the BRI. For countries and organisations to “join” the BRI, China and the respective country or organisation sign a Memorandum of Understanding (MoU).

For the five countries listed in official Chinese media (yidaiyilu.gov.cn), we could not confirm a signature of an MoU for bilateral cooperation under the Belt and Road Initiative framework.

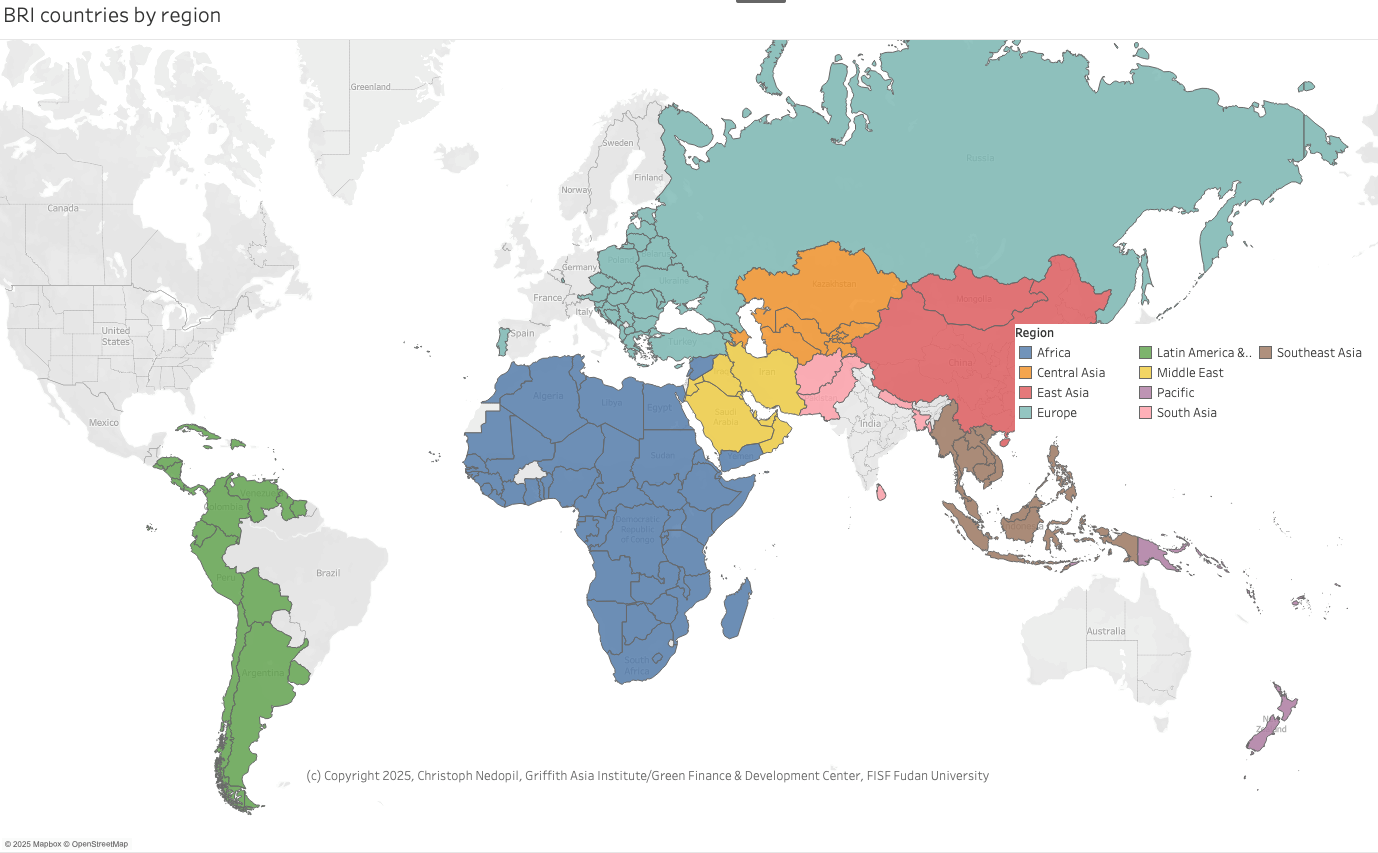

The following BRI map shows the list of countries that have signed MoUs or are considered members of the BRI, organised by region as used in this report. A more detailed list of BRI countries can be found here.

.

About the author

Dr Christoph NEDOPIL is the Director of the Griffith Asia Institute and a Professor at Griffith University in Brisbane, Australia. He is also a Visiting Professor at FISF Fudan University, Shanghai, Acting Director of the Green Finance & Development Center at FISF Fudan University, and a Visiting Faculty at Singapore Management University (SMU).

Christoph regularly provides advice to governments, financial institutions, enterprises, and civil society on sustainable development issues. He is the lead author of the UNDP SDG Finance Taxonomy, the Innovative Climate Finance Solutions report for the G20 in Indonesia, and the Green Development Guidance of the BRI Green Development Coalition under the Chinese Ministry of Ecology and Environment. He has authored four books and published articles in Science and other leading journals. Christoph serves as a board director in scaling sustainability in businesses and finance.

Christoph is quoted regularly in Financial Times, The Economist, Reuters, Bloomberg, and other major outlets. Before joining Griffith University, he served as Founding Director of the Green Finance & Development Center and Associate Professor at the Fanhai International School of Finance (FISF), Fudan University and previously as Founding Director for the Green BRI Center at the Central University of Economics in Beijing. He worked with the World Bank in over 15 countries and was a Director in the German development agency GIZ. Christoph holds a Master of Engineering and a PhD in Economics from the Technical University Berlin, as well as a Master of Public Administration from Harvard Kennedy School.

About Griffith Asia Institute

Griffith Asia Institute (GAI) at Griffith University, Brisbane, Australia, is an internationally recognised institute providing knowledge, and solutions for sustainable development in Asia-Pacific. With a history of over 20 years, GAI has forged strong partnerships with key decision-makers in business, policy and with research institutions across the region. With over 80 faculty members and 50 adjunct members, GAI works in multidisciplinary teams and draws on a wide range of technical expertise in energy, finance, policy, and economics as well as in regional studies including a strong China component.

GAI is led by Professor Christoph Nedopil and is organised through knowledge and regional hubs:

The Green Transition and Sustainable Development Hub addresses major challenges and opportunities for Asian and Pacific economies in addressing SDGs related to climate, life on land, life in the sea, partnerships, infrastructure and energy.

The Governance and Diplomacy Hub addresses major challenges and opportunities in the region for peaceful co-existence, diplomacy, inclusive governance, policymaking and institution building.

The Inclusive Growth and Rural Development Hub addresses major challenges and opportunities in the region regarding currently underserved communities (e.g., women, indigenous, youth, rural, or people with disabilities).

The four regional hubs address major regional and country-specific challenges and opportunities in (1) Southeast Asia, (2) South Asia, (3) Pacific and (4) China and the Region, each with their own hub lead.

About the Green Finance & Development Center

The Green Finance & Development Center (GFDC) is a leading research centre that provides advisory, research and capacity building for financial institutions and regulators for green and sustainable finance in China and internationally.

The GFDC works at the intersection of finance, policy, and industry to accelerate the development and use of green and sustainable finance instruments to address the climate and biodiversity crisis, as well as contribute to better social development opportunities.

The topics of our work at the Green Finance & Development Center respond to the needs and developments of the financial markets and related policies in China and internationally, while we also aim to provide evidence-based advisory and research for future policies and strategies to accelerate the greening of finance in policy and practice.

The Green Finance & Development Center was founded in 2021 by Christoph Nedopil when he worked in Fudan International School of Finance (FISF) at Fudan University in Shanghai, PR China.

Notes and references

[1] Nedopil, C. (2025). Countries of the Belt and Road Initiative (BRI). Green Finance & Development Center, FISF Fudan University. https://greenfdc.org/countries-of-the-belt-and-road-initiative-bri/

[2] For comparison reasons: if only including deals larger than USD 100 million as was done before 2024, construction engagement would be USD 124.4 billion and investments would be 82.6 billion USD, with a total engagement of 207 billion – a relatively minor difference.

[3] Ministry of Commerce (MofCom). (2025, December 24). Investment and cooperation between my country and countries participating in the Belt and Road Initiative from January to November 2025. Ministry of Commerce (MofCom) Going Global Website. https://fec.mofcom.gov.cn/article/fwydyl/tjsj/202512/20251203613450.shtml

[4] Scissors, D. (2023). China Global Investment Tracker 2023 (China Global Invest ment Tracker). American Enterprise Institute (AEI). http://www.aei.org/china-global-investment-tracker/

[5] For comparison reasons with slightly different data collection approaches since 2024, the analysis focuses on deal size larger than USD100 million in this analysis (see About Data section on first page). If all deal sizes including those smaller than USD 100 million are included in this calculation, the deal size for investment was USD 587 million and USD 626 million for construction contracts.

[6] For a definition of the regions, see the map in Appendix 2.

[7] Boway Alloys Plans to Invest No More than US$150 Million to Build a Production Base in Morocco, Diverting Its Overseas Exports to Morocco., 2025

[8] Wu, J. (2025, February 26). LONGi Seal €7.6 Billion Deal For Green Hydrogen Project in Nigeria [Substack newsletter]. China Hydrogen Bulletin. https://chinahydrogen.substack.com/p/longi-seal-76-billion-deal-for-green

[9] ChinaChina Yonghua and Congo (Brazzaville) sign a $23 billion oil and gas development agreement—Seetao. (2025, September 8). Seetao. https://www.facebook.com/sharer/sharer.php?u=https%3A%2F%2Fwww.seetaoe.com%2Fdetails%2F248787.html

[10] Penny, E. (2025, August 4). The 1H2025 investment matrix | Data centres take FDI by storm. Fdi Intelligence. https://www.fdiintelligence.com/content/9f01314f-cff5-4bf1-9bd3-8daa177a6668

[11] Measuring foreign direct investment. (2025, November). OECD. https://www.oecd.org/en/topics/foreign-direct-investment-fdi.html

[12] UNCTAD (United Nations Conference on Trade and Development). (2025, October 31). Global foreign investment falls 3% in first half of 2025, hitting industry and infrastructure. https://unctad.org/news/global-foreign-investment-falls-3-first-half-2025-hitting-industry-and-infrastructure